Two Ways to Build an AI Power Grid: China's State Model vs. America's Market Bet.

The American approach to AI infrastructure is, at its core, a financial story. China has a different word for what it's building: state infrastructure.

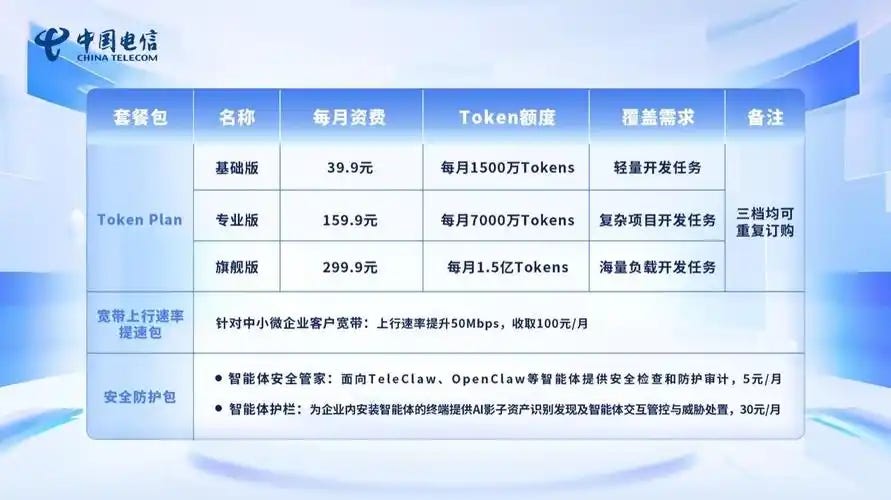

Last week, China Telecom started selling AI tokens the same way it sells mobile data — monthly subscription plans, starting at $1.40 for 10 million tokens. China Mobile and China Unicom followed immediately. China Telecom’s chairman said the company must shift ‘from traffic operations to token operations.’ China Mobile has already made compute services one of its three core businesses alongside communications and smart services.

This is worth pausing on. The largest telecom operators in the world’s most populous country just decided that selling compute is their core business. Not phone calls. Not data plans. AI tokens. This didn’t happen because the market drifted there. It happened because the Chinese state decided compute is infrastructure, and then organized its state-owned carriers accordingly.

A few days before those subscription plans launched, a ceremony took place in Wuxi — a manufacturing city in Jiangsu province that most Westerners have never heard of. Hongxin Electronics signed a contract to deploy four Huawei Ascend 384 supernode servers, each one delivering 300 petaflops of compute at BF16 precision. The project has a name: Token Factory. The goal is to build the largest Huawei AI compute cluster in East China.

These two things — a telecom company selling token subscriptions and a factory in a second-tier city deploying supernode clusters — are not separate stories. They are the same story. China is building a compute grid, modeled on its national electricity grid, and it is moving fast. The difference between how fast China is moving and how fast America is moving comes down to something simpler than technology: it is about who is making the decisions and why.

The American approach to AI infrastructure is, at its core, a financial story. OpenAI raises capital from Microsoft. Anthropic raises from Amazon and Google. Meta spends its own profits. Each company builds its own data centers, buys its own chips, runs its own models, and charges for access. The system generates impressive technology. American frontier models are technically ahead. But the system also has a structural ceiling built into it, because the people running it make more money when AI is expensive. American AI companies sell tokens, and the more compute each token requires, the more they can charge. The four major American labs — OpenAI, Anthropic, Google DeepMind, and xAI — all run closed models. They do not share research on efficiency because efficiency cuts into margins. They are vertically integrated with the cloud providers who fund them, which means anyone who wants to compete with them needs permission from a competitor to access the compute to do it. Five companies end up setting the pace for the entire industry. In China, the dynamic runs in the opposite direction. DeepSeek publishes its research openly. Labs share efficiency techniques across the industry. The models are mostly open source. When you cannot buy unlimited compute, you have every incentive to let others help you squeeze more out of what you have.

The Chinese approach starts from a different premise. On April 28th, the Politburo issued a statement calling for accelerated construction of six national infrastructure networks: water grids, power grids, compute grids, communications networks, urban pipe networks, and logistics networks. Compute grid. Right there between water and electricity. In Chinese policy language, being named in a Politburo statement is not an announcement. It is an instruction that cascades down through every level of government, state bank, and state-owned enterprise until things get built. According to NDRC chairman Zheng Shanjie, speaking at the National People’s Congress press conference in March 2026, investment in these six networks would exceed 7 trillion yuan — roughly $970 billion — in 2026 alone

This is not the first time China has organized around a strategic technology this way. In the early 2000s, China decided solar panels were infrastructure. The state directed capital to manufacturers, subsidized land and electricity, mandated purchasing from utilities, and produced companies at a scale no private market would have funded. The result was that China now makes roughly 80 percent of the world’s solar panels. The same pattern ran through electric vehicles, where state subsidies, purchasing mandates, and protected domestic markets turned BYD from an obscure battery maker into the world’s largest EV company. And through semiconductors, where SMIC and others received direct state equity investment, preferential loans, and guaranteed procurement contracts from state-owned enterprises. You can argue about the trade-offs of this model. You cannot argue that it does not produce scale fast.

Compute is the next item on that list.

The Huawei chip story is where the geopolitics gets interesting. Before the U.S. export controls, Chinese AI companies used Nvidia GPUs. Everybody did. Nvidia’s chips were faster, better supported, and the entire AI software ecosystem was built around them. Huawei’s Ascend chips existed as a backup option. Then the U.S. restricted the H100. Then the H800. Each time China found a path forward, the controls tightened. The intended message was: the chips will stop coming, so stop planning around them. What happened instead is that Chinese engineers, with no other option, started actually learning the Ascend platform. Software got ported. Bugs got fixed. China Mobile placed an order for roughly 6,200 Ascend AI accelerator cards worth about $2.8 billion, specifically locking in the Huawei ecosystem. The export controls were designed to function as a wall. They functioned as a forcing function. Necessity plus state procurement contracts is a recipe China has used before. It is how COMAC built a domestic commercial aircraft. It is how Huawei built its own chip fab capacity after being cut off from TSMC. Whether the resulting products match their Western equivalents immediately is beside the point. The point is that the dependency gets removed.

Why a City You’ve Never Heard Of

Most Western coverage of Chinese tech focuses on Beijing, Shanghai, and Shenzhen — cities with university research ecosystems, venture capital, and a startup culture that maps onto a familiar template. Wuxi does not fit that template, and that is exactly what makes it interesting. Wuxi’s economy is built on precision manufacturing: electronics enclosures, cooling systems, semiconductor packaging, the physical components that go into devices. When the Chinese state decided that modular AI data centers — built fast, deployed at scale, shipping 60-megawatt units globally within months of contract signing — were a strategic priority, the question was where the supply chain to build them already existed. The answer was Wuxi. The local government put together a dedicated project team, ran approval processes in parallel, and went from signed agreement to groundbreaking in four months. In a market system, capital flows to where returns are highest. In a state-directed system, capital flows to where the national plan requires. For physical compute infrastructure, these two destinations are often different places.

The deepest difference between the two systems, though, is not about speed or location. It is about what each system is optimizing for. The American system optimizes for financial value. This sounds like a criticism, but it is mostly just a description. American AI companies are valued in the hundreds of billions of dollars. Their investors include the largest asset managers and sovereign wealth funds on earth. Their goal is to maximize that valuation, and the mechanisms for doing so — closed models, vertical integration with cloud providers, expensive tokens, concentration in a few major labs — are entirely rational given the incentive structure. The incentive is to build scarcity, not abundance. Cheap and universal access to AI is good for users. It is not particularly good for earnings. The end result is a system that is very good at generating financial value and structurally resistant to generating broad access.

The Chinese system is organized around a different goal: deploying technology across the entire economy, not just in sectors where returns are high enough for private capital. Part of what makes this possible is that China channels an unusually large share of its national income into investment rather than consumption. According to World Bank data, Chinese household consumption sits at roughly 40 percent of GDP, compared to around 67 percent in the United States. That gap — the portion of the economy that in America would flow back to households as spending — flows instead into infrastructure, industrial capacity, and strategic technology. It is how China built the world’s largest high-speed rail network, the world’s dominant solar manufacturing industry, and now, the compute grid. Whether you view this as a collective investment or a structural constraint on Chinese households depends on your vantage point. What is harder to dispute is the output.

The token subscription plans from China Telecom, China Mobile, and China Unicom are the consumer-facing product of this system. 9.9 yuan per month for 10 million tokens. Less than a cup of coffee for access to the country’s AI compute infrastructure. This is not a promotional discount. It is a policy implementation. The state decided that AI compute should be a utility, organized the carriers to deliver it, built the grid to run it, and priced it accordingly. Whether the underlying technology is as good as OpenAI’s is almost secondary to the question of what happens to an economy when every factory, hospital, school, and small business can access AI inference for the price of a streaming subscription.

America’s answer to that question is still being formulated. The assumption has been that market competition will eventually drive prices down and access up, the same way it happened with cloud computing. That assumption may be correct. It may also be the kind of assumption that looks reasonable right up until a competitor builds the grid first.

In Wuxi, four Huawei supernode servers are being installed in a building they are calling a Token Factory. The chips are domestic. The financing is state-backed. The policy framework came from a Politburo statement. The supply chain came from thirty years of building electronics factories in Jiangsu. The U.S. tried to prevent this with export controls. China accelerated instead. What is becoming clear is that the world may not converge on a single model for AI infrastructure. One is built by markets, priced for returns, and concentrated in a handful of companies. The other is built by states, priced as a utility, and treated as national plumbing. Both are now running. The competition between them is just getting started.

| A guest post by

|