Don't Watch the Robot. Watch What It Can't Move Without.

The supply chain and industrial ecosystem often matter more than the headline-grabbing videos.

Every week, another humanoid robot video appears from China.

A robot walks through a factory carrying components. Another folds clothes on a table. Another performs on a stage in front of a crowd. The videos are impressive. But they show only the final product, the part of the story that’s easiest to film.

The harder question is what makes those robots possible.

Building a humanoid robot is not purely an AI challenge. It is a manufacturing challenge: precision components that almost no one can make at scale, specialized suppliers operating near capacity, factories capable of driving costs down fast enough to create a real market, and an industrial ecosystem that can bring all of it together. The robot is the headline. The industrial system behind it is the story.

The Robot is a Bag of Parts

Start by taking the machine apart.

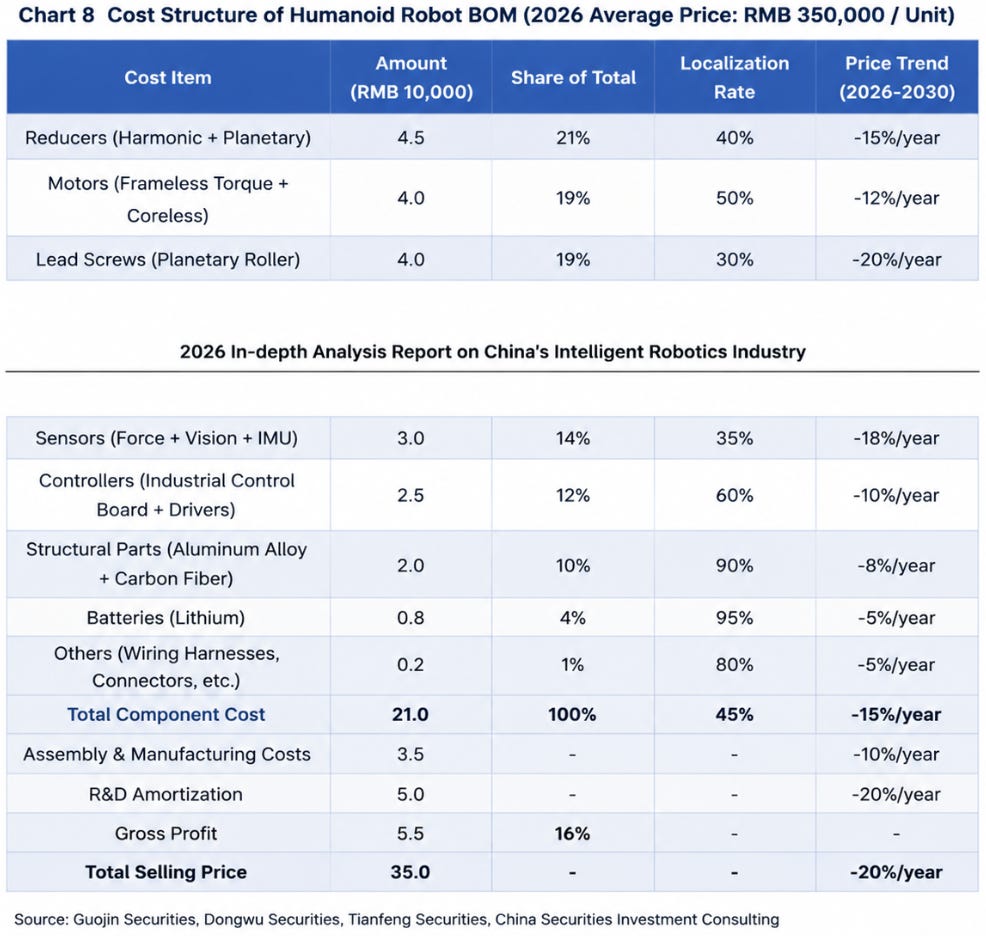

According to a 2026 industry analysis by China Securities Investment Consulting, a humanoid robot at an average price of around ¥350,000(USD51,707) breaks down into a surprisingly small number of cost categories: precision reducers at 21% of the bill of materials, motors at 19%, lead screws at 19%, sensors at 14%, controllers at 12%, and structural parts at 10%. Six categories. That’s 95% of what you’re paying for.

The robot body, the thing that appears in the video, is the assembly. And assemblies commoditize. China’s humanoid average selling price are expected to fall toward ¥100,000-¥150,000(USD14,773-USD22,160) by 2030. Unitree’s G1 already starts at ¥99,000(USD14,625). Zhiyuan’s Expedition A2 lists at ¥200,000(USD29,547). UBTech’s Walker S sits at ¥500,000(USD73,868) and is already running inside automotive factories.

This is the same arc as the laptop, the smartphone, the EV. The device gets cheap fast. The parts that make it work do not.

Unitree became famous because its robots dance. The more interesting question is why it can sell a humanoid robot at a fraction of what Boston Dynamics charges. The answer is not that Unitree is smarter. It’s that Unitree sits inside a supply chain ecosystem that Boston Dynamics doesn’t, one where motors, controllers, structural parts, and sensors can be sourced domestically, iterated rapidly, and repriced downward with every production run. The dance is the marketing. The supply chain is the business.

Which means the real question isn’t who builds the most impressive robot. It’s who controls the components the robot can’t function without, and whether China has the industrial base to make those components at scale, at cost, without depending on Japan, Switzerland, or the United States.

The answer, right now, is complicated. And the complication is the whole story.

The Smile That Shows You Where the Money Goes

China’s industrial analysts have a name for the profit structure of the robotics supply chain: the smile curve. The two ends, upstream component makers and downstream system integrators, capture the high margins. The middle, the robot body itself, is where value gets compressed.

Upstream component makers currently capture some of the highest margins in the robotics industry. According to China Securities Investment Consulting’s analysis, specialized component makers can achieve margins of 30–50%. Robot body manufacturers, the companies that dominate most headlines, operate on much thinner margins of around 10–15%. Downstream system integrators that sit closer to customers and accumulate deployment data and experience can command margins in the 20–40% range.

But this curve is not static. As robot production scales and key components become increasingly standardized, the industry’s profit pool is expected to shift upward. Hardware will face growing commoditization: component suppliers will see margin pressure as domestic alternatives improve, while robot manufacturers will compete in a market where the physical machine itself becomes less differentiated.

The biggest shift will happen higher in the stack. AI algorithms, operational software, and deployment data currently represent a relatively small share of the industry’s economics, but their importance will grow rapidly as robots move from controlled environments into complex real-world applications. By 2030, these layers could capture around 40% of the industry’s economic value, becoming the most defensible and highest-margin part of the robotics ecosystem.

The companies that survive the next decade are not the ones that built the most impressive robot in 2026. They’re the ones that own either end of the smile: the upstream components that can’t be replicated, or the data and software stack that compounds with every additional unit deployed.

China’s position on the left end of that smile, the upstream components, is more complicated than anyone in either the bullish or the bearish camp wants to admit.

The Parts That Decide Who Wins

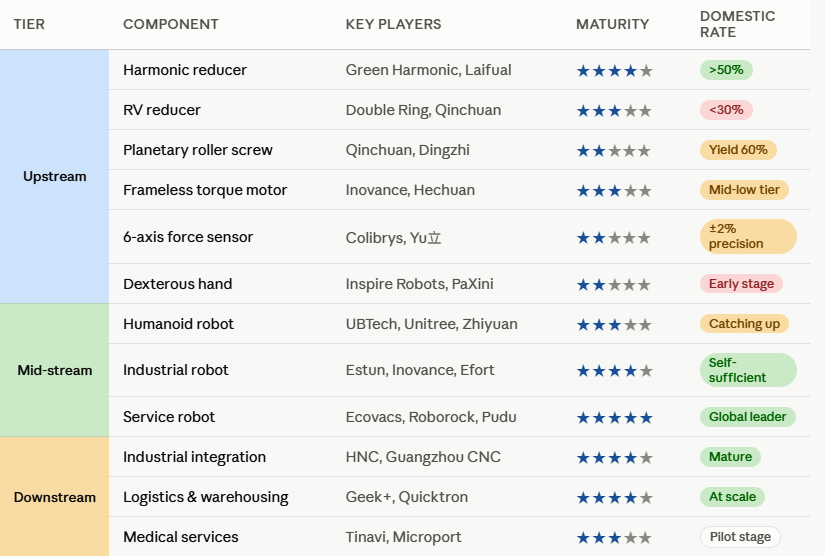

A humanoid robot looks like an AI product. But manufacturing one looks much closer to building an electric vehicle: hundreds of suppliers, thousands of precision parts, and a brutal requirement for cost reduction at every level of the stack. There are four component categories where the manufacturing challenge is hardest, the supply is most concentrated, and the competitive outcome is most uncertain.

The reducer nobody can easily copy.

Every rotary joint in a humanoid, shoulder, hip, knee, elbow, needs a precision reducer. The reducer trades rotational speed for torque and eliminates backlash. An arm that wobbles a millimeter can’t thread a bolt. A knee joint that slips under load collapses the robot mid-step. A single humanoid carries 10–14 reducers, and they represent 21% of total unit cost, the largest single line item on the bill of materials.

For decades, Japanese companies have controlled the joints of industrial robots. Harmonic Drive Systems owns the small-joint harmonic gear market. Nabtesco owns the large-joint RV reducer market and together they hold roughly 80% of global supply. The standard line in the industry is that a real disruption at either company would halt robot production at most major manufacturers on the planet.

China’s position on reducers is split. On harmonic reducers, used in lighter joints like wrists and forearms, it has made genuine industrial progress. Green Harmonic (绿的谐波) holds roughly 60% of the domestic market and has extended product lifespan to around 15,000 hours, a level that matches or exceeds Harmonic Drive Systems’ benchmark, and it now ships to Tesla’s Mexico production line. The company says humanoids account for 30% of its revenue. Domestic harmonic reducers have crossed 50% market share inside China. This is a real industrial achievement.

RV reducers, the heavy-load joints at the robot’s base and upper arms, are a different story. China’s domestic production rate sits below 30%, and the precision requirements of humanoid applications remain largely import-dependent. The gap is not a design gap. It’s decades of accumulated process knowledge in materials, heat treatment, and precision grinding that cannot be transferred through a reverse-engineering exercise.

The reducer story in one sentence: China solved the easier half and is still working on the harder half. The harder half is 21% of everything.

The screw China cannot yet make at scale.

This is the component almost no one outside the industry discusses, and it may be the most consequential near-term bottleneck.

Humanoid linear joints, the actuators that push, absorb shock, and power the limbs, don’t run on ordinary ball screws. They run on planetary roller screws. The distinction matters: a ball screw concentrates load on a single track of bearings. A planetary roller screw spreads it across dozens of simultaneous contact points. That’s the difference between a joint that walks reliably for a year and one that strips under repeated loading in weeks.

China leads the world on rotary actuators. On planetary roller screws, domestic yield remains around 60%, compare with 85%+ among Swiss and European leaders like Rollvis and GSA. The gap is materials and process: steel purity, thread grinding precision, heat treatment consistency, inspection equipment. Qinchuan Machine Tool and Dingzhi Technology are investing aggressively, and the industry projects domestic yield crossing 80% by 2027–2028.

But right now, every Chinese humanoid that ships contains a critical linear joint component that largely comes from abroad. The country that controls rare-earth magnets does not yet control the screw. That asymmetry is the most honest description of where the supply chain actually stands.

The sensor measured in decimal places.

A humanoid needs to feel. The six-axis force-torque sensor, typically four to six per robot at wrist and ankle positions, measures forces and torques in three dimensions simultaneously. It tells the robot how hard it’s pushing, whether it’s about to drop something, whether the surface it’s contacting is yielding.

The precision gap is exactly as wide as it sounds. Domestic Chinese sensors achieve ±2% full-scale accuracy. ATI of the US and Kistler of Switzerland achieve ±0.5%, a fourfold difference in measurement precision. In precision assembly or medical applications, that gap determines whether a robot is commercially viable or just a demonstration.

Chinese manufacturers have made inroads in collaborative robots and consumer electronics manufacturing, where precision requirements are lower. But the high-precision humanoid tier remains foreign-supplier dominated. At ¥5,000–30,000 per unit, across four to six units per robot, sensors represent 14% of total cost, and the precision shortfall constrains the addressable application range of every robot that ships with domestic components.

The hand that nobody has solved.

Save the hardest for last.

The cost structure of a humanoid robot changes depending on how the system is broken down. At the component level, reducers, motors, lead screws, sensors, and controllers represent the largest individual cost categories. But when viewed as a functional subsystem, the dexterous hand becomes one of the most expensive modules, accounting for roughly 31% of total humanoid BOM cost because it integrates precision actuators, sensors, and control systems.

The reason is simple: the human hand is an engineering masterpiece. It contains around 17,000 tactile receptors, can detect slips as small as 0.1mm, and respond to tiny changes in force. The best robot hands in 2026 remain far behind biology, with leading systems achieving roughly millimeter-level tactile resolution and 0.1N-level force precision. Current domestic Chinese humanoid hands typically operate with 6–11 degrees of freedom.

This is why almost every humanoid robot demonstration still looks slightly unnatural. The hardest problem is not walking. It is the hand.

The market has already priced this as the decisive bottleneck. Outside the race to build complete humanoid robots, hand-focused companies are attracting serious investor attention. Linker Robot (灵心巧手) focuses exclusively on dexterous hands, attaching them to existing industrial arms rather than building full humanoid bodies, and reportedly reached a valuation approaching ¥10 billion. PaXini Technology, another hand-focused company, reportedly raised a ¥1 billion Series A round.

The market is saying: whoever solves the hand doesn’t just win a component contract. They unlock every application that currently remains out of reach.

The hand is the bottleneck inside the bottleneck. No one, anywhere, has solved it yet.

What the Component List Misses

Four chokepoints explains the hardware. It doesn’t explain the system.

China’s advantage in robotics is not a supply chain. It is an ecosystem, and an ecosystem has layers that a component breakdown can’t capture.

The first layer is components. That’s what we just covered, and China’s position is mixed: strong on some inputs, import-dependent on others.

The second layer is manufacturing capability, the precision machining, tooling culture, and supply chain coordination density that exists in China at a scale unmatched anywhere. This is the layer that took the EV from prototype to 10 million annual units in less than a decade. Those same factories, those same tooling engineers, that same supply chain muscle now applies to robots. When a humanoid company needs to iterate its actuator design, the turnaround time inside China’s manufacturing base is weeks, not quarters. That speed compounds.

The third layer is deployment. China has the application environments: automotive factories actively seeking labor flexibility, 3C electronics manufacturers that need adaptable assembly lines, hotel and restaurant chains already running service robots at commercial scale. Each real-world deployment generates data. Data trains better models. Better models justify the next deployment. The loop is self-reinforcing, but only if you have the deployment base to start it.

The fourth layer is capital and government coordination. And this is the one most outside observers consistently underestimate.

Liuzhou is a third-tier city in Guangxi province. By conventional metrics it has no business being a robotics hub. Its main claim to industrial significance is the SAIC-GM-Wuling joint venture that produces China’s best-selling EV. But what Liuzhou did with UBTech tells you something important about how China’s robot ecosystem actually assembles itself.

The Liuzhou government didn’t offer a tax rebate and call it industrial policy. It invested directly in UBTech’s equity through state-linked funds, putting itself on the company’s cap table. It signed a collaboration agreement with a local automotive factory to train UBTech’s humanoids directly on a live production floor. And it built its own robot training data center, a facility where humans demonstrate physical tasks to robots, collecting the embodied AI training data that every robot company needs to improve its models.

Then it planned to resell that data to other robotics companies.

A city government in Guangxi built infrastructure to generate robot training data, positioned itself as a supplier to the broader robotics industry, and used that capability as a recruitment pitch to attract more companies. Liuzhou is not just a node in the hardware supply chain. It is positioning itself as a node in the AI training data supply chain.

This is what China’s local government playbook looks like as the old tools get constrained. Under anti-involution policies introduced to limit destructive local subsidy races, the straightforward options, tax rebates, land grants, direct cash payments, are harder to deploy. What’s replaced them is direct equity investment. And equity investment changes the dynamic in a specific way: a government with a stake on the cap table doesn’t just want a factory in its city. It needs returns. That pressure forces companies toward revenue faster than they might otherwise move.

The result is uncomfortable and productive at the same time. Robots get deployed before they’re fully ready. Deployments generate real-world data that lab testing can’t produce. The data improves models. The models justify the next deployment. A third-tier city in Guangxi ends up holding training data assets that no amount of compute budget can simply purchase.

What to Actually Watch

Not the backflip. The backflip is marketing.

Watch the RV reducer domestic market share. It sits below 30% today. When it crosses 40%, the import dependency on Japan that represents 21% of total humanoid cost begins to break, and the economics of every Chinese-built machine shift permanently.

Watch the planetary roller screw yield rate. At 60% today, targeting 80% by 2027–2028. When domestic production reaches that yield at meaningful volume, the last major linear motion import dependency closes.

Watch six-axis force sensor precision. At ±2% today, targeting ±1% by 2027 and ±0.5% by 2028. Each precision threshold unlocks a new tier of applications, industrial assembly first, then medical, then household.

Watch the dexterous hand degrees of freedom. At 6–11 today, targeting 20 by 2028. The hand is the single component that determines whether humanoids remain in structured factory environments or become genuinely versatile.

And watch what local governments build, not the subsidy announcements, but the infrastructure. Data centers collecting robot training data. Equity positions creating commercialization pressure. Factory trial partnerships generating real-world deployment data that no simulation can replace.

The robot is the headline. The reducer yield rate, the screw tolerance, the sensor precision, and the training data center in Guangxi are the story.

China isn’t building a better robot. It’s building a system where every layer, components, manufacturing capacity, deployment environments, capital, and government coordination, pushes in the same direction simultaneously. The chokepoints inside that system are real. The domestic supply chain has genuine gaps. But the ecosystem being constructed around those gaps is the more durable competitive position.

And the ecosystem, unlike the robot, is very hard to replicate from the outside.

Don’t watch the robot. Watch what it can’t move without. Then watch who built the infrastructure that makes it possible to manufacture those things, at scale, at falling cost, in China, without asking anyone’s permission.

| A guest post by

|