Why China Is Falling Behind in the Space Race

Blocked from SpaceX, China is building its own commercial space fleet, but funding gaps and strict rules may keep it from ever catching up.

On June 12, a friend texted me good news: through Rakuten Securities in Tokyo, he had won an allocation of SpaceX shares. From a hotel room in Dongguan, I tried to open SpaceX’s website. All I got was Error 1009. So I switched over to SpaceLens, a Chinese spaceflight outlet streaming on Bilibili, where a host was narrating SpaceX ringing the opening bell on Nasdaq.

My friend and I are both Chinese. The difference is that he studies in Japan.

A week before SpaceX’s $75 billion IPO, users in mainland China and Hong Kong could no longer reach the company’s website. According to Bloomberg, the banks leading the deal had decided that regulatory risk made it impossible to let clients in Hong Kong and China—private-banking customers included—into the offering. Japanese investors, by contrast, were handed a $2.5 billion allocation.

Musk threw a party for global investors. The Chinese, plainly, were not on the list.

(This piece sets aside SpaceX’s merger with xAI and the company’s effect on broader market stability. I’m interested only in the rockets and the satellite-internet business.)

One Law, 28 Years of Fallout

The easy explanation for China’s exclusion is that you cannot invest in a company that builds for the U.S. military. But that’s too easy. In the 1990s, China was an enthusiastic player in the commercial launch market. It even put a Hughes communications satellite into orbit.

What changed was a man named Christopher Cox (He also used to chair the SEC — by all accounts, did a decent job). The California congressman argued that American firms had leaked technology to China, and that China had used commercial launches to acquire missile-guidance know-how. The fallout was the tightening of the International Traffic in Arms Regulations, or ITAR, in 1998.

The effect was sweeping: any spacecraft containing U.S.-made components could no longer ride a Chinese rocket. Commercial communications satellites were reclassified as military-adjacent technology—even if the only thing a given satellite did was beam television—which all but barred Chinese firms from taking foreign commercial satellite orbits. (Independently developed research satellites were exempt.)

Under ITAR, the disclosures in SpaceX’s prospectus can themselves be read as a technical document. Rather than untangle the compliance risk, the underwriters drew a hard line around China.

The law’s bite is not theoretical. After ITAR tightened, China carried out no commercial launches at all from 1999 to 2005. It did not resume delivering satellites for foreign customers until 2024.

Chinese Faces in SpaceX Promo Videos

Here’s the part that surprises people. Despite ITAR, SpaceX employed a fair number of Chinese nationals for years. Right up until the Starshield program began in 2022, Chinese engineers holding U.S. Green cards worked actively on SpaceX projects. A few Chinese faces also appeared in the company’s promotional videos.

I asked a Chinese aerospace professional about this. (He requested anonymity, citing a conflict of interest.) He said some of those employees flowed back to China after 2022. The rest were rerouted into engineering work that touched no sensitive technology. After the xAI merger, some of the engineers building Grok now count, on paper, as part of SpaceX—but they have nothing to do with the space business.

Even setting policy aside, SpaceX pay sits below what Chinese candidates expect. According to the same source, a new graduate at SpaceX earns $60,000 to $70,000 a year and is expected on-site at least five days a week, sometimes roused at 2 a.m. to respond. A Silicon Valley software engineer, by comparison, often starts above $100,000—a far cushier landing.

Which is how a Chinese dad-joke was born: Don’t worry, son. We’ve got a SpaceX at home, too.

“Don’t worry, son. We’ve got a SpaceX at home.”

At the end of 2014, China’s State Council issued “Document 60,” opening the launch and satellite-manufacturing sectors to private companies. Starlink didn’t exist yet, but SpaceX was already reliably ferrying cargo to the International Space Station.

The document followed a familiar Chinese growth recipe: watch a frontier industry, find the stable leader, write policy to encourage imitators, then let enough private firms run free inside controlled bounds.

For a while it worked. A wave of commercial-space startups appeared. Then came a brutal five-year shakeout. Underfunded companies died; on social media, commercial space briefly looked like a scam. Only between 2020 and 2022 did a stable roster of players finally emerge:

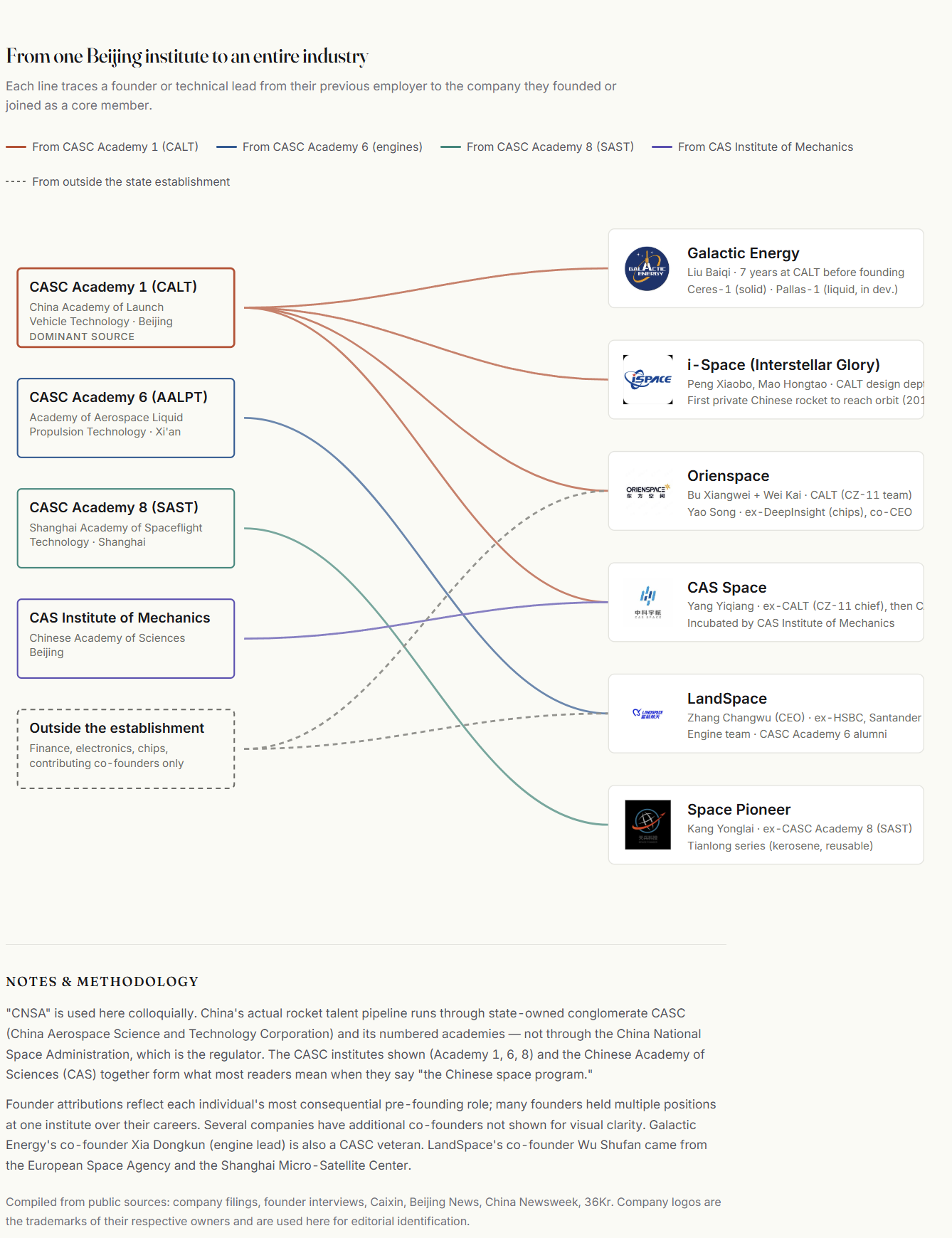

Rockets: LandSpace, Space Pioneer, iSpace, Galactic Energy, CAS Space, Orienspace

Remote-sensing imagery: Chang Guang Satellite

These firms started fast for one decisive reason: most of their founding teams came out of China’s state aerospace institutes.

The founders of iSpace, Galactic Energy, Orienspace and CAS Space all came from CALT, the academy responsible for overall launch-vehicle design. Part of LandSpace’s team came from the institute that develops rocket engines; Galaxy Space’s technical core came from China’s main satellite-design academy; Chang Guang’s people came from the Changchun optics institute. A founder from an aerospace institute meant a deep bench of talent—and a more investable company. At the time, Chinese venture capital was fixated on the internet and electric cars and barely touched space, so the firms that survived were simply the ones with the most engineers.

Luck Ran Out

China’s commercial-space sector then drew a bad hand. COVID, beginning in 2020, broke the rhythm of test flights and fundraising. Real engineering deliveries didn’t start arriving until 2023.

That year was a breakthrough. Space Pioneer’s Tianlong-2 reached orbit. CAS Space’s Lijian-1 set a domestic record by carrying 26 satellites on a single flight. And LandSpace’s Zhuque-2 became the first methane-fueled rocket anywhere to reach orbit.

If all you cared about was getting something up, Galactic Energy’s Ceres series could already fly often. The catch is that Ceres is a small solid-fuel rocket: under one ton to low orbit, often below 500 kilograms. A solid rocket is essentially a missile—once it fires, the engine isn’t coming back. You launch it once and you’re done.

To cut launch costs, most Chinese firms chased methane. Methane burns more cleanly than the kerosene SpaceX uses, leaving less carbon buildup inside the engine and making the rocket easier to refly. As latecomers, these companies wanted to leapfrog SpaceX. Space Pioneer was the exception, sticking with kerosene for its Tianlong series, which—mirroring the Falcon 9—reaches a claimed 17 tons to low orbit. In other words, a Chinese Falcon 9.

But haste has its price. None of these attempts has fully worked. Tianlong-3 broke apart after launch. Zhuque-3 flew but failed to land its booster. Everyone else’s liquid rockets are still early—mostly at the engine hot-fire stage. China conducted 92 launches in 2025; the only two failures both came from private companies, which dragged the whole sector behind schedule.

China Doesn’t Have Enough Rockets

Too few private launches hits China’s satellite-internet ambitions first. To field a Starlink rival, China is building two mega-constellations: Guowang (GW) and Spacesail. GW needs 12,000 satellites; Spacesail needs more than 15,000. Both broke ground in late 2023 and needed heavy private-rocket cadence by 2024.

Then, in June 2024, a Tianlong-3 engine tore loose from its test stand, flew into the air, and came down on a nearby hillside. The accident pushed private spaceflight into roughly half a year of silence. By January 2026, GW had more than 150 satellites in orbit and Spacesail more than 200—together just 1 to 1.5 percent of the planned totals.

And the clock is unforgiving. Between 2020 and 2024, China filed for more than 50,000 low-orbit satellites with the International Telecommunication Union. In late 2025, it filed for more than 200,000 more. ITU rules require launching a first satellite within seven years, deploying 10 percent within nine, and finishing within 14—or forfeiting the spectrum. That means China must orbit more than 20,000 satellites by 2034, and it is throttled by how rarely it can launch.

Even with a perfect cadence, China lacks the rockets. Take LandSpace’s Zhuque-3. Assume it flies cleanly: in reusable mode it can lift close to 18 tons, or about 16 tons of satellites once you subtract the dispenser. A first-generation Spacesail satellite weighs 300 kilograms; a production GW satellite, 300 to 500. So one rocket might carry 30 to 50 satellites—call it 25 to 40 with margin. Twenty thousand satellites then demand 500 to 800 Zhuque-3 flights. Over eight years, without reuse, that’s 65 to 100 launches a year. LandSpace’s current Zhuque-3 capacity is 20 a year. Reuse helps cut how many you must build—but recovery itself takes time.

Not every rocket will have Zhuque-3’s lift, either, so factor in the smaller vehicles and the real demand climbs. A source says China’s planned commercial rocket count may reach 3,000. Long term, that’s an opportunity. Short term, it’s a severe shortfall.

Why Is China Being so Careful?

How did it get this way—and how long until “China’s SpaceX” actually catches SpaceX?

Here’s the surprise: the Chinese formula of fierce internal competition and rapid mass production, which closed the gap on the U.S. in so many industries, did not replicate in space. The likely reason is that Musk already ran that playbook himself. SpaceX cut its teeth competing with United Launch Alliance; NASA funded it precisely to break the ULA-and-Boeing monopoly. SpaceX flew repeatedly from 2008, and from 2015 proved reusability through a long string of tests. Musk had already done the hard, iterative, Chinese-style middle stage.

China’s government, by contrast, has been unusually conservative here—and the reason is partly Qian Xuesen, the father of the Chinese space program. After the first Dongfeng-2 missile failed, Qian articulated the “reset to zero” principle: pin down the exact cause of a failure, reproduce it, and durably fix the whole class of problem—then, on the management side, trace how the error happened, hold the responsible parties accountable, and tighten the process.

That doctrine became spaceflight’s iron law. Every failure runs the full procedure. For missiles and crewed flight, the slow, meticulous discipline is exactly right. But China applies it to commercial space as a whole-industry reset: one company’s rocket fails, and everyone halts to hunt for the cause. It spares China the workplace injuries and explosions of SpaceX’s move-fast era—but each reset freezes the sector while engineers go looking, and the delays starve the system of launch capacity.

On top of that, commercial missions must queue behind the government’s crewed flights and research launches. To protect the official science calendar, some commercial missions wait or slip, squeezing their launch windows further.

This produces a counterintuitive conclusion: Chinese commercial space loses money because it launches too rarely. Too few flights, and rockets can’t cycle through reuse efficiently, so component costs stay high. Launches are likelier to fail, so customers can’t trust them. The result is a death spiral—failure, halt, lost faith, harder fundraising. A company needs a launch success rate above 95 percent to commercialize, and that requires a lot of flights.

Small Budget, Big Ambitions

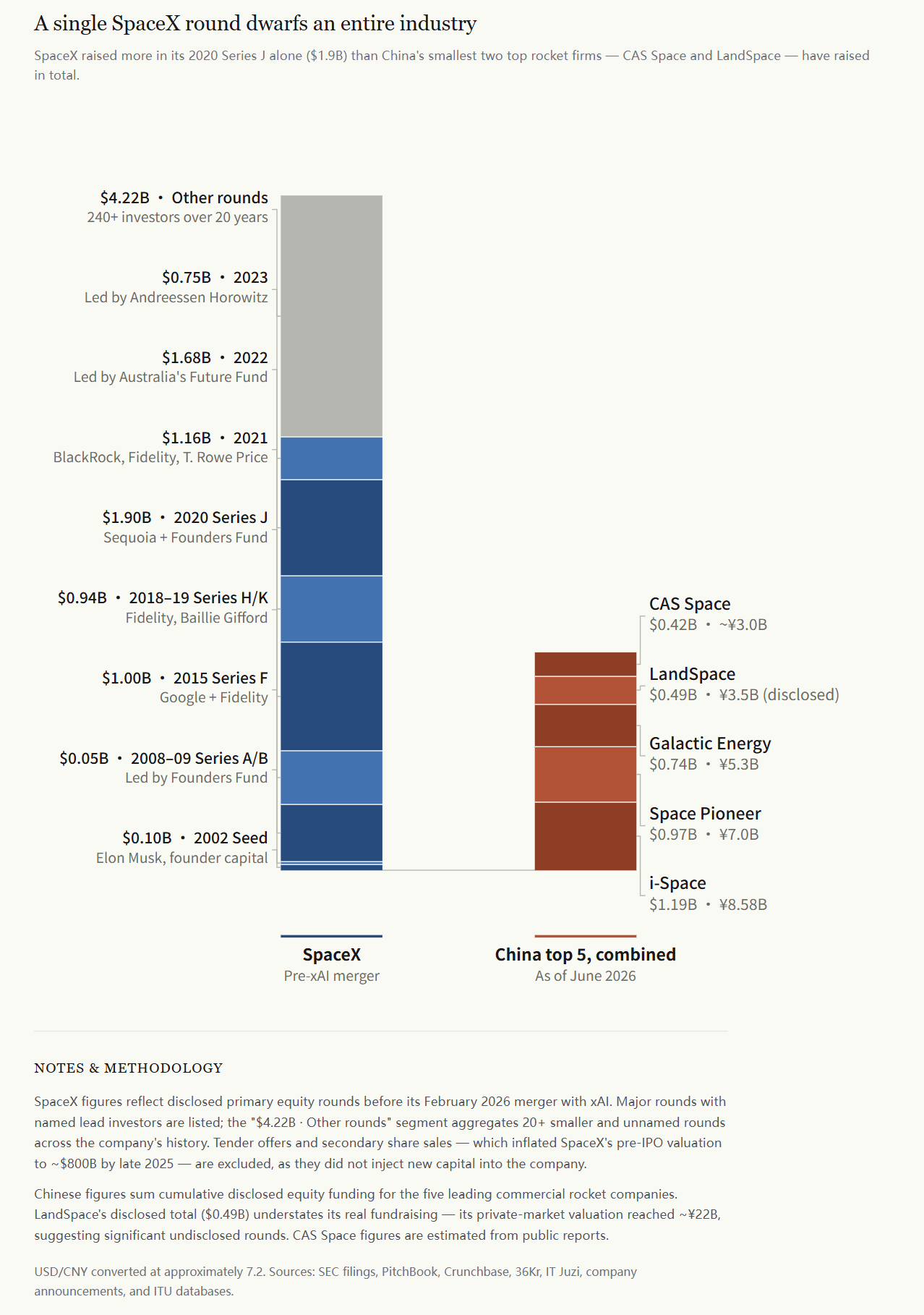

Against SpaceX, Chinese firms have one more problem: not enough cash. SpaceX was a lucky company. It started with a $100 million infusion from a man who was already rich (now a trillionaire), which bought it room to operate. Since 2002, its disclosed private-market fundraising runs to about $12 billion.

The Chinese players don’t come close. LandSpace, nearing its IPO, has closed fundraising at more than $1 billion. iSpace raised over $1.1 billion this year. Galactic Energy took in more than $700 million last September. Space Pioneer’s cumulative raise is about $840 million. Across the board, Chinese commercial rocket firms have raised only around 10 percent of what SpaceX did—and even if Chinese manufacturing can compress costs, that gap won’t close fast.

A source in the field estimates the entire Chinese commercial-space industry has now raised about $10 billion cumulatively. “Investors are stuck with nowhere to put their money,” he said, “because the rocket companies have stopped raising—they’re getting ready to list.”

By his reckoning, SpaceX effectively absorbed more than $140 billion in disguised investment through NASA crewed-flight contracts and Defense Department satellite launches. “A program like Starshield can carry a $40 billion framework,” he said. NASA, through the Artemis program, has poured money into Starship. “Starship has already spent $15 billion, and NASA is betting on it to reach the moon—but it still hasn’t produced anything of value.”

There’s a structural gap, too: China has no company that does both rockets and satellites the way SpaceX does. The appeal of that integrated model is obvious—SpaceX commands roughly 90 percent of the world’s launch payload by mass, while Starlink has more than 7,000 satellites in orbit. Chinese firms remain scattered, with no vertical integration.

The reason is mundane. Fully testing one engine can take five to ten years, and most rocket companies can’t wait that long. So they buy engines from state institutes and assemble around them—but buying an engine is nothing like shopping at a market. Aerospace component prices in China are opaque, and because the orders are so small, the prices run high. Components that can’t get cheaper leave no room for profit.

“If you want batteries for an electric-pump rocket, automotive batteries might actually perform better,” said the anonymous source. “But a space company might use a few hundred cells, while a carmaker orders tens of thousands. Nobody wants the space company’s business.”

Is There A Turning Point?

SpaceX has more than 10 million users across roughly 100 countries. But its service is brushing against its ceiling. According to OpenSignal, within 12 months of Starlink entering Indonesia, congestion cut download speeds by nearly two-thirds and uploads by almost half—downloads fell from 42 Mbps in 2024 to 15.8 Mbps in 2025, uploads from 10.5 to 5.4. The cause was a demand surge: users poured in faster than local capacity could be built out.

And it isn’t only Indonesia. As Starlink subscribers spike across India and Africa, the pattern may become routine. Industry analysts argue that Starship’s lack of commercialization is holding Starlink back. “Only the Starlink V3 satellites deliver better service, and Falcon can’t loft them,” one said. “And Starship—well, you’ve seen what it looks like.”

There’s an opening here. Temidayo Oniosun, CEO of the tracking firm Space in Africa, told Rest of World that African governments are welcoming new entrants. With no competition, he noted, Starlink has raised prices repeatedly after winning share—and city dwellers may now be hunting for an alternative.

Musk’s own politics are loosening Starlink’s grip in some markets, too. In 2024, after he refused to comply with a Brazilian court’s content-moderation order against X, the platform was banned for five weeks—an opening for Spacesail. When Starlink declined to meet Kazakhstan’s data-security requirements, its project to connect 2,000 schools there stalled in 2024.

That handed Spacesail a chance. In November 2024 the constellation struck a deal with Brazil’s state telecom; the country’s regulator granted Spacesail an operating license the following February. Spacesail signed with Malaysia’s Measat in 2025. Other Chinese firms, such as Galaxy Space, are prioritizing Southeast Asia.

Still, Chinese companies care most about the home market. Most are angling for satellite-comms contracts with China’s three big carriers, or for in-car connectivity. “In China, a model like the AITO M9 already has satellite comms built in,” one analyst said. “Spacesail chasing foreign markets is, in a way, a sign of weakness. GW has finished its first networking phase and will be more competitive.” He, too, asked not to be named.

For now, the latest deadline for China to build its own SpaceX looks like 2028 to 2030. The Chinese don’t have much time.

Coda

I like watching frontier industries and talking to the people inside them. My personal list of “frontier industries” right now is commercial space, robotaxis, flying cars and humanoid robots. (I’m a cautious skeptic of large language models and the internet sector.) So I report on these fields in China and invest in them—I’m no professional, but the investing tends to pay.

As a journalist, I once helped livestream the launch of Orienspace’s Gravity-1 rocket. The on-site conditions were, twice, nearly a disaster. The first time, the local network kept dropping. The second time, heavy rain made it impossible to film the rocket directly. And yet, when you hear the roar in person, you feel, from somewhere deep, the greatness of what humans can do.

That’s why I follow these industries: the application of advanced technology makes me happy. But commercial space is the most conservative of China’s frontier sectors in its pace.

That has to do with “military-civil fusion.” Every aerospace professional I spoke to was as candid as they could be—and every one of them, without exception, asked to remain anonymous in this story. Inside China or abroad, disclosure invites needless trouble, so they keep quiet to avoid it. What produces that confusion is, precisely, a geopolitics complex enough to swallow everything around it.

One last thing. As I finished writing, my friend’s SpaceX shares had passed $200. He has no plans to sell. “Maybe I’ll pass them down to my son,” he said.

| A guest post by

|