Why Chinese AI's Richest Story Isn't About Revenue

Kimi earns. DeepSeek dominates. Zhipu listed first. So why does the market keep getting the rankings backwards?

Ask a developer which Chinese AI model they’re running today, and the answer is almost always DeepSeek. Ask which one they use for reading dense documents or running agents, and Kimi comes up. Ask about Z.ai and you’ll get a respectful nod, maybe a mention of GLM, then a pause. Technically strong, they’ll say. Just not the first thing that comes to mind.

Yet when you look at the capital flowing into these three companies, the developer conversation and the investor conversation seem to be happening in completely different universes.

In rapid succession, three events put Chinese AI’s value squarely in the spotlight. According to an exclusive report by LatePost, Moonshot AI, the company behind Kimi chatbot,is closing a $2 billion funding round led by Meituan Dragon Ball, pushing its post-money valuation to $20 billion , the most successful fundraise by any independent Chinese AI startup to date. Almost simultaneously, DeepSeek opened its doors to outside investors for the first time: according to The Information and Reuters, it is targeting up to $7.35 billion in its first external round, at a valuation that sources place at up to $50 billion though the final number could still change as talks are ongoing. And Z.ai, which had already beaten both of them to the finish line, listing on the Hong Kong Stock Exchange in January at a market cap that would surge past HK$300 billion($38.3 billion)within weeks, making it the world’s first publicly traded large language model company — watched from the sidelines as the market’s attention flowed elsewhere.

Three companies. Three very different moves. And a set of numbers that don’t add up the way you’d expect.

Here’s the paradox that nobody has quite explained cleanly:

Kimi has $200 million in annual recurring revenue, a figure disclosed by Meituan Dragon Ball’s partner to LatePost, who reported that Kimi’s ARR crossed $100 million in early March and surpassed $200 million by April, driven by accelerating paid subscriptions and API usage. Its valuation: $20 billion. DeepSeek has never disclosed its revenue, prices its API at one-tenth of OpenAI’s rates, and 127 million monthly active users — fourteen times Kimi’s. Its reported valuation: up to $50 billion, roughly 2.5 times Kimi’s with talks still ongoing. Z.ai went public first, carries Tsinghua’s institutional prestige, and spent years methodically building government contracts. Its market reception: underwhelming by comparison.

The company making the most money is worth the least. The company that refuses to talk about money is worth the most. And Z.ai, the one that crossed the finish line first — is the company every institution believes in and every developer forgets to mention first.”

This isn’t irrational. It’s a story about three completely different ways of thinking and how those ways of thinking translate, or fail to translate, into the stories that capital markets reward.

Three Companies, Three Instincts

The valuation gap makes no sense until you look at where each company comes from, not geographically, but intellectually.

DeepSeek is the quantitative trading firm. Its parent, High-Flyer, is one of China’s most successful quant funds. The culture that built High-Flyer is the same culture running DeepSeek: obsessive about signal quality, indifferent to narrative, rigorous about long-term compounding, and deeply suspicious of short-term incentive structures. Founder Liang Wenfeng spent years refusing external investment not because he couldn’t get it, but because outside capital would have introduced a clock — LP timelines, board pressure, quarterly expectations — that he didn’t want running in the background while he was trying to think clearly about training efficiency.

The quant instinct is: find the edge that nobody else has found, run it at scale, and don’t explain it until you have to.

Moonshot is the VC-backed startup. Yang Zhilin came up through the conventional Silicon Valley-adjacent innovation ecosystem, raised early from tier-one investors, and structured Kimi from day one as a company that would need to tell a compelling story to sophisticated capital repeatedly. That’s not a criticism, it’s a skill set. Yang protected his technical control through dual-class share structures and brought in Zhang Yutong as President specifically to manage the relationship with capital that he didn’t want to manage himself. When Alibaba came in with roughly $800 million — partly as cloud compute credits, partly as cash, according to Alibaba’s annual filing with the Hong Kong Stock Exchange— Kimi navigated a complex negotiation involving competing interests from Alibaba, Tencent, and a growing roster of strategic investors. That navigation required a founder culture comfortable with capital complexity.

The VC instinct is: build something real, tell the story clearly, grow the metrics, raise the next round.

Z.ai is the academic research lab. Born from Tsinghua’s Knowledge Engineering Lab under Professor Tang Jie, Zhipu’s foundational logic is the logic of the institution: produce excellent research, train excellent people, establish credibility through rigor, and let quality speak for itself. The team is disproportionately Tsinghua graduates. Decision-making flows through academic consensus. The instinct toward first-principles thinking is strong; the instinct toward market responsiveness is weaker.

The academic instinct is: do the work correctly, and recognition will follow.

Why the VC Instinct Produces a Lower Valuation

Kimi is genuinely impressive by conventional startup metrics. It crossed $200 million in ARR, a figure its investors, Meituan Dragon Ball, chose to disclose publicly, which itself signals that they’re using revenue as a valuation justification rather than a future aspiration. Paid subscriptions are growing. API revenue is accelerating. The commercialization machine is running.

But here’s the problem with being a legible, well-run startup: investors can model you.

Kimi has $200 million in ARR and a functioning business, which means investors can model it. And a company that can be modeled has a ceiling. That ceiling, according to LatePost, is $20 billion.

Legibility is a ceiling.

Kimi’s commercial success also comes with strings attached. Alibaba invested roughly $800 million for what was then approximately a 36% stake- a share that has since been diluted through multiple subsequent rounds, though Alibaba remains one of its most significant backers. Tencent,which simultaneously holds Kimi equity and is reportedly in discussions with DeepSeek has its own strategic interests. Every investor on the cap table has a thesis, and those theses don’t always point in the same direction. The money that built Kimi is also the money that constrains it. More capital means more complexity means more demands on management attention that could be going toward the technology.

The VC model works. But it produces a company whose valuation is bounded by the conventional frameworks investors apply to companies that work.

DeepSeek’s Edge: The Value of Being Unmodelable

DeepSeek’s approach to money looks, from the outside, like indifference. In practice, it is something more strategic: the deliberate avoidance of premature legibility.

For years, Liang Wenfeng kept DeepSeek’s revenue private, kept its API prices at a fraction of competitors’, and kept releasing its models as open source. This strategy is not optimized for short-term revenue. It is optimized for something the quant mind understands well: market position that compounds over time.

127 million monthly active users, built without a marketing budget, without a consumer app ecosystem, without the distribution advantages of being owned by ByteDance or Alibaba — is a number that cannot be fully explained by the quality of the models alone. It reflects an ecosystem strategy: make the models cheap enough that developers build on them, open enough that they spread, and good enough that switching away becomes painful. The DeepSeek API runs at roughly one-tenth of OpenAI’s pricing. That’s not a business model. It’s a land grab.

Now state capital is reportedly entering. China’s National Integrated Circuit Industry Investment Fund is in discussions to lead DeepSeek’s first external fundraise, which would value the company at over $51.5 billion. The moment that happens, DeepSeek stops being a research lab with a quant fund patron and starts being national AI infrastructure. And national AI infrastructure is not valued like a startup. It is valued like a strategic asset — which means the conventional frameworks don’t apply.

The quant tribe built something that the market cannot fully model. That illegibility is not a bug. It is precisely why the valuation is higher.

Z.ai Listed First — and the Stock Exploded. So Why Does Nobody Talk About It?

Z.ai did everything in the right order. It built on decades of Tsinghua research. It established early technical credibility with ChatGLM-6B, which became the first Chinese open-source model that ordinary developers could run on consumer hardware. It methodically raised 16 rounds of funding. It went public on the Hong Kong Stock Exchange in January 2026 — the first large language model company anywhere in the world to list.

And the stock market’s response was emphatically not “fine.” Within 43 days of listing, Z.ai’s share price had surged over 500% from its IPO price of HK$116. By April it briefly crossed HK$1,000, making it one of Hong Kong’s rare four-digit stocks, with a market cap exceeding HK$300 billion($38.3 billion), larger than JD.com and Kuaishou, closing in on Baidu. In April 2026, Time Magazine named it one of the world’s ten most influential AI companies. Investors and institutions clearly believed in it.

So here is the more precise version of Z.ai’s tension: it is not that the capital markets ignored it. It is that the developer community’s imagination did.

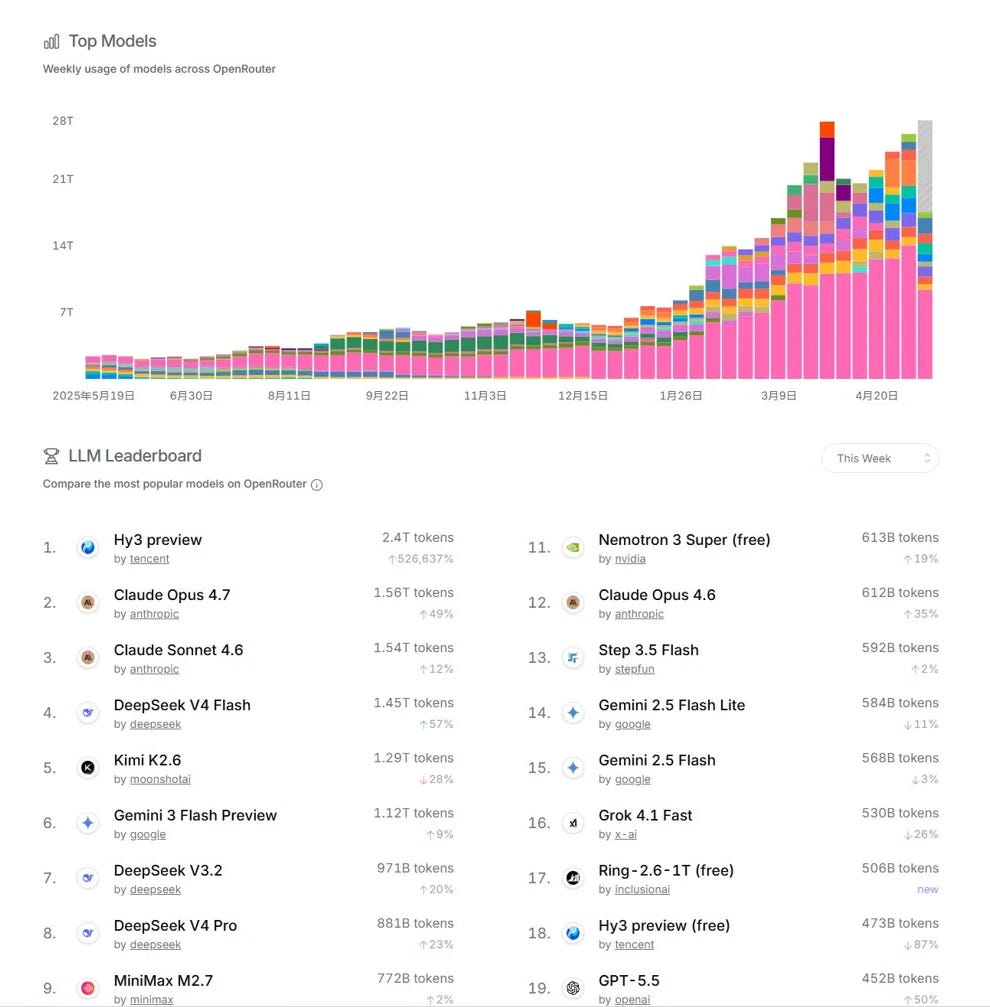

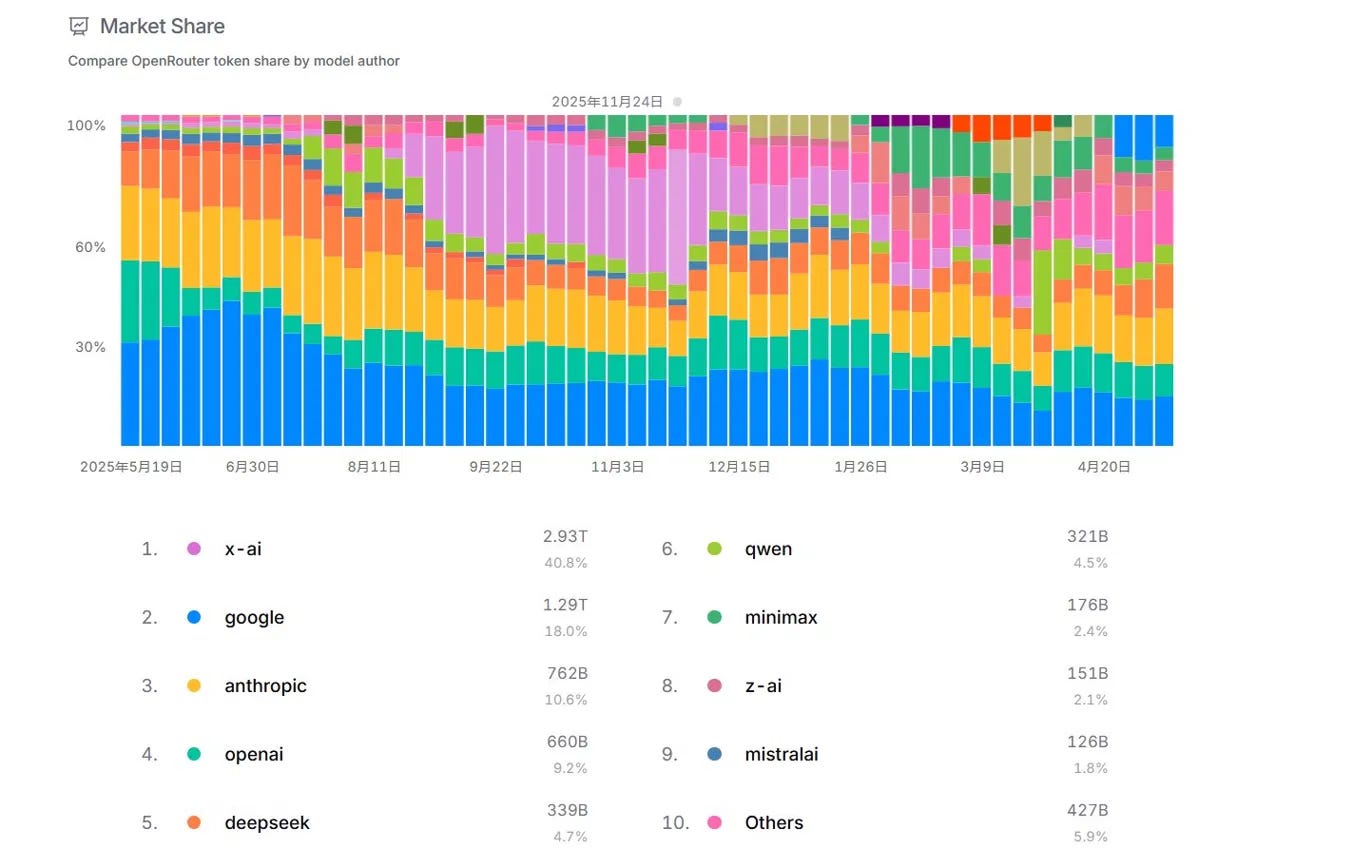

The contrast with its two peers is stark. DeepSeek has become the default reference model in developer conversations worldwide, the “price-performance king” and open-source benchmark for coding, math, and reasoning tasks. On OpenRouter, Hugging Face, and across international developer forums, its discussion volume and actual usage stickiness are exceptionally high. Many industry observers simply call it the new standard. Kimi, meanwhile, has carved out a loyal following in long-context and agent use cases — researchers, lawyers, financial analysts who need to process dense documents reach for it instinctively. On OpenRouter’s usage rankings, it frequently sits near the top.

Z.ai’s GLM-5.1 is technically competitive with both. On SWE-Bench Pro and real-world coding tasks, it holds its own against the best open-source models globally, and in some agent and multimodal benchmarks it leads the field. Its platform already serves over 700,000 enterprise and developer accounts. By any rigorous technical measure, it belongs at the table.

But belonging at the table and owning the conversation are different things. Browse developer selection guides, Zhihu threads, CSDN discussions, or international AI comparisons, and a pattern emerges: DeepSeek and Kimi appear as the headline act; Z.ai appears as the reliable third option. Not dismissed, respected, even but consistently positioned as the “serious enterprise player” rather than the one generating excitement. In international English-language coverage, DeepSeek’s low-cost shock moment and Kimi’s K2 breakthroughs get standalone treatment; Z.ai more often appears in ensemble pieces about China’s “AI Tigers,” rarely as the lead.

This is the academic instinct’s specific blind spot: it is very good at impressing the people who read carefully, government buyers, enterprise procurement teams, benchmark judges but less naturally wired for the kind of messy, fast-moving developer enthusiasm that spreads a model organically. When Manus triggered an agent frenzy, Z.ai rushed out AutoGLM; users found it underwhelming. Being thorough and being quick are different skills, and Tsinghua culture optimizes for the former.

This is not a story of failure. GLM-5.1’s technical reception among professional developers is genuinely improving. Its enterprise customer base is large and loyal. Its public listing gives it a financial cushion that most competitors would envy. These are real advantages that don’t show up in Twitter threads.

But AI ecosystems have a specific compounding logic: the models developers talk about get integrated into products, which generates real-world usage data, which makes the next version of that model better, which makes more developers choose it. It is a self-reinforcing loop. DeepSeek and Kimi are inside that loop. Z.ai is watching from the edge of it. A rising stock price tells you what institutional investors thought of your last three years. Developer gravity tells you who gets to shape the next three.

What the Valuation Gap Is Actually Measuring

The gap between Kimi’s $20 billion, DeepSeek’s $51.5 billion, and Z.ai’s HK$300 billion($38.3 billion)-plus public market cap tells three different stories — and none of them are primarily about current revenue or model capability. What they are measuring is narrative optionality: how many different futures an investor can plausibly imagine when they think about each company.

When investors look at Kimi, they see a well-run AI startup. The futures they can imagine are the normal startup futures: growth, consolidation, potential acquisition, potential IPO at a larger multiple. These are good futures. They are also bounded futures.

When investors look at DeepSeek — especially a DeepSeek with state backing — they can imagine something larger: the default API layer for Chinese enterprise AI, the model that developers everywhere build on because it’s the cheapest and increasingly the best, the technical infrastructure that makes China’s AI ecosystem less dependent on American compute. These futures are not guaranteed. But their potential scale is enormous, and their valuation logic escapes conventional modeling.

When investors look at Z.ai, they see a technically credible company that the Hong Kong market has already richly rewarded — and is now asking a harder question: does the stock price reflect a future that the industry narrative hasn’t yet caught up to, or does the gap between capital market enthusiasm and ecosystem presence signal something the stock hasn’t yet priced in?

The Clock That Changes Everything

Here is the thing about the valuation paradox: it is temporary.

DeepSeek’s first external fundraise starts a clock. External LPs have return expectations. State capital has strategic timelines. The Information reported that DeepSeek will accelerate commercialization following the round, with V4.1 adding enterprise-specific tooling. The company that has spent years avoiding the pressures of external capital is about to discover what Kimi already knows: every dollar raised is also a deadline.

Kimi’s $200 million ARR is not just a metric. It is a preview of the questions DeepSeek will be asked in 12 to 18 months: What is your retention? What is your enterprise pipeline? When do you break even?

And Z.ai, having already crossed into public markets, is living in that future right now — answering quarterly, in public, for every strategic choice it makes.

Three companies. Three instincts. Three different relationships with the clock.

The quant tribe built the biggest valuation by refusing to be legible on anyone else’s timeline. The VC tribe built the best business by learning to speak capital’s language fluently. The academic tribe went public first, watched its stock surge 500% in six weeks, and is now confronting the question that capital market success defers but doesn’t answer: do developers reach for you first, or only when the other options aren’t available?

The question is not which valuation is correct today. The question is which instinct survives contact with the same set of pressures — because eventually, all three companies will face them.