Who Pays for AI? How America and China Are Monetizing AI Differently

Silicon Valley is selling productivity. China is selling reach. The gap between them explains more about the AI race than any benchmark ever could.

When ByteDance announced subscription tiers for Doubao (68 yuan, 200 yuan, or 500 yuan per month), the response in China was swift and largely hostile. “I’ll delete the app.” “More expensive than ChatGPT.” The backlash trended on Weibo for days.

Stop and think about that for a second.

ChatGPT Plus has been charging $20 a month since 2023. Claude Pro costs $20. Google AI Pro costs $20. Nobody in the US wrote think pieces about whether AI chatbots deserve to charge. The question was never really contested.

So why does Doubao charging roughly $10 a month feel like a provocation in China while the same price point in America is just... Tuesday?

The easy answer is “Chinese users are used to free internet.” That’s true, but it’s also incomplete. The more revealing answer comes down to one distinction, one that cuts through almost all the noise about models, benchmarks, and market share:

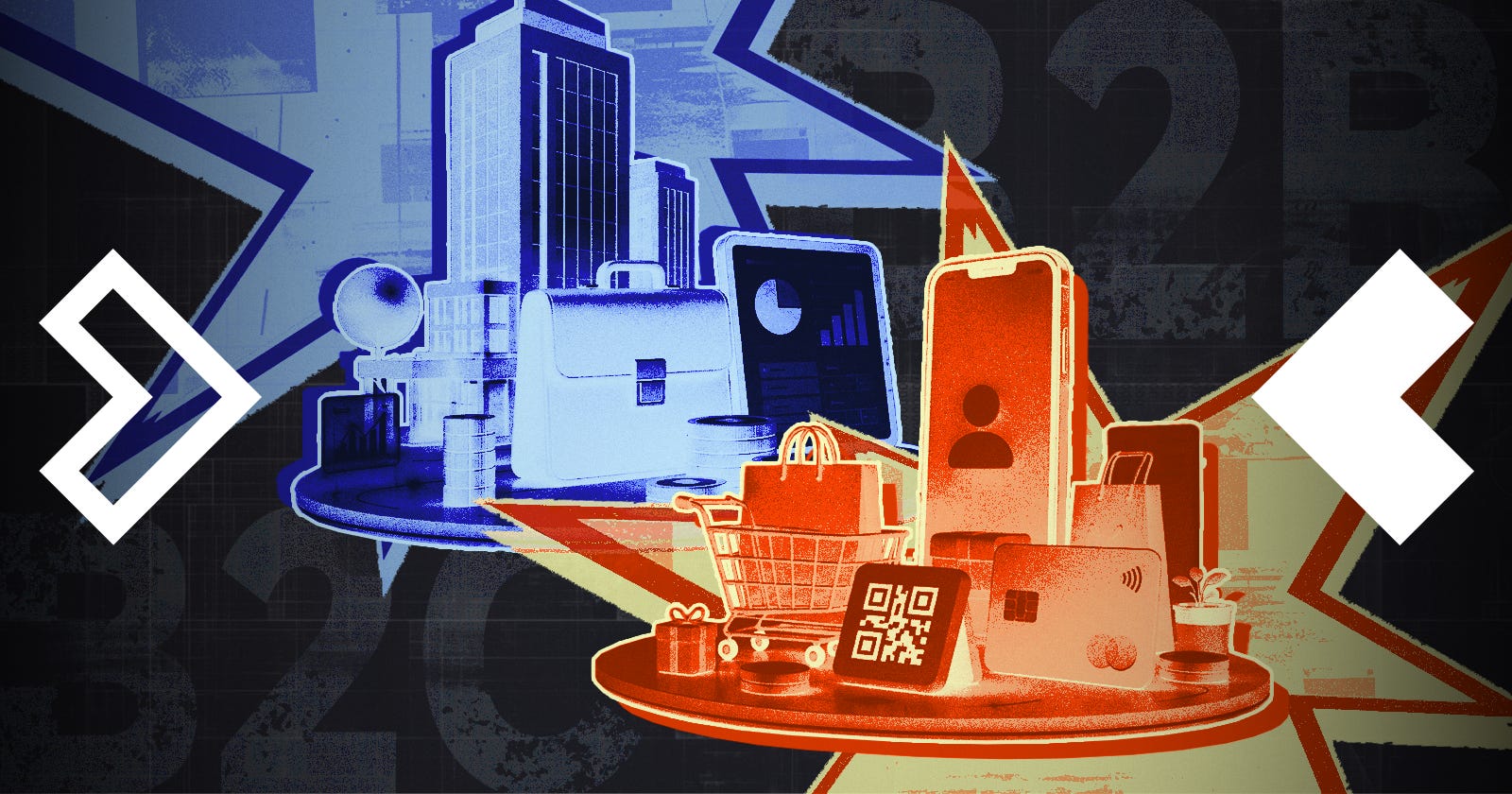

American AI companies have found a way to monetize through enterprises. Chinese AI companies have been competing through consumers.

Those are two completely different statements. One is about where the revenue comes from. The other is about what the competition looks like. And the gap between them explains not just why 68 yuan caused a Weibo storm, but why the entire AI industry on each side of the Pacific looks so structurally different.

Two Different Scoreboards

There’s a framing that gets thrown around a lot: American AI is more “B2B” while Chinese AI is more “B2C.” It sounds intuitive. It’s also wrong, or at least it misses the point.

OpenAI has hundreds of millions of monthly active users. ChatGPT is arguably the most successful consumer AI product ever built. That doesn’t sound very B2B. Doubao has 345 million monthly active users in China, a number that any American consumer tech company would kill for. That doesn’t sound very B2C either, if B2C implies actually charging consumers.

The real distinction shows up in what each industry chooses to measure.

In the US, the coverage that moves markets is about annual recurring revenue, enterprise customer counts, and API revenue growth. Anthropic recently disclosed that approximately 80% of its revenue comes from business and API customers, serving over 300,000 companies. More than 1,000 of those now spend over $1 million annually. When Anthropic’s annualized revenue crossed $30 billion in April 2026, the story wasn’t user growth. It was the speed of enterprise adoption.

In China, Bytedance’s Doubao, Kimi, and Alibaba’s Qwen compete on a completely different scoreboard. The metrics that matter are downloads, DAU, and MAU. In early 2026, Chinese media breathlessly covered Doubao crossing 100 million daily active users. Nobody was asking about ARR.

Two different scoreboards. Two different industries.

The Real Reason: It’s Not Just SaaS History

The standard explanation for this divergence points to commercial history: the US has a mature enterprise software culture (Microsoft 365, Salesforce, Snowflake), while China’s internet giants built their empires on advertising, e-commerce, and gaming. Not SaaS.

That’s true. But it’s background, not root cause.

The deeper reason is what each country’s AI products actually do for the people paying for them.

American AI products (ChatGPT, Claude, Cursor, Claude Code) have penetrated labor markets. A law firm deploys Claude to accelerate document review. A software team uses Claude Code to ship features faster. A consulting firm runs ChatGPT Enterprise to cut research time. In each case, the value is concrete and quantifiable: hours saved, headcount avoided, output increased. The ROI calculation is straightforward enough that a CFO can sign off on it.

American AI companies are monetizing labor.

Chinese AI companies are monetizing attention.

That distinction is not really about what the products can do. Chinese AI products (ByteDance’s Doubao, Alibaba’s Qwen, Kimi, Tencent’s Yuanbao) are often used for the same tasks as their American counterparts — writing, research, image generation, and answering questions. The difference is who pays and why.

In the United States, the users converting into paying customers tend to have a measurable ROI calculation. A lawyer bills more hours. A developer ships code faster. A consultant spends less time on research. The value is tied directly to output — which is what makes a $20 monthly subscription feel like a business expense, and a six-figure enterprise contract defensible in a procurement meeting. American AI companies are not simply selling intelligence; they are selling productivity gains that enterprises can measure and justify.

In China, the value is often real but harder to quantify. AI makes daily life more convenient, more efficient, and more enjoyable, but not necessarily in ways that fit neatly into a procurement budget or a subscription calculation. As a result, Chinese AI companies have largely competed for consumer attention first — maximizing reach, engagement, and user scale before figuring out how to monetize them.

That is why China’s leading AI companies are increasingly looking beyond subscriptions and toward commerce. The bet is that if users are reluctant to pay directly for intelligence, merchants may pay for transactions generated through it. The Qwen–Taobao integration and the Doubao–Douyin commerce loop are not simply product features. They are attempts to convert attention into transactions — and transactions into revenue.

To be fair, this doesn’t mean Chinese AI companies ignore enterprises. Alibaba, Baidu, ByteDance, and Tencent are all investing heavily in enterprise AI. But the details matter.

Zhipu (GLM), which went public in Hong Kong in January 2026, derives 85% of its revenue from enterprise clients. Yet much of that business comes from government agencies, state-owned enterprises, and financial institutions purchasing private deployments — a model structurally different from the broad-based commercial demand driving companies like Anthropic.

MiniMax tells the opposite story. Roughly 71% of its revenue comes from consumer applications, primarily its AI companion app Talkie and video generator Hailuo.

DeepSeek sits somewhere in between. Despite becoming China’s most internationally recognized AI lab, it has barely begun monetizing. Its aggressive API price cuts look more like a land-grab strategy than a mature revenue model.

The broader point remains: while Chinese AI companies are pursuing enterprise customers, none has yet demonstrated the kind of large-scale, recurring enterprise demand that now sits at the center of Anthropic’s business.

Why China Is Betting on Commerce

The revenue models that worked for Chinese internet companies (advertising, e-commerce commissions, gaming) don’t map cleanly onto AI chatbots. You can’t put banner ads in a conversation. You can’t run a flash sale in a reasoning engine.

So the question becomes: what monetization model does China actually know how to scale?

The answer the industry has converged on is commerce. The reason becomes clear when you look at what these companies actually are at their core.

ByteDance built its empire on short-video and social commerce through Douyin. Alibaba’s foundation is e-commerce: Taobao, Tmall, and payments through Alipay. Their AI chatbots, Doubao and Qwen respectively, were never going to be standalone products. They’re new entry points into existing transaction ecosystems. Tencent’s Yuanbao is being positioned the same way, as a gateway into WeChat’s social and payment infrastructure.

This explains the AI commerce arms race that has defined 2025 and 2026. Doubao integrated with Douyin Commerce and completed a full in-app transaction loop by April 2026. Qwen fully connected with Taobao in May 2026, giving users access to 4 billion products and enabling purchase completion without leaving the app. The revenue model in both cases is CPS (cost per sale), where the platform takes a commission on transactions flowing through the AI interface.

The bet is coherent: if you can’t charge users for the intelligence, charge merchants for the transaction. Commerce may be the only monetization model China already knows how to scale.

The open question is whether it works. The AI commerce funnels are still small, the transaction volumes early-stage, and the habit formation unproven. Meanwhile, the player with the clearest structural advantage in this space is Tencent. WeChat brings 1.4 billion monthly active users, trusted payment rails, and a mini-program ecosystem covering millions of merchants. It hasn’t fully deployed yet. When WeChat Agent launches, it may reset the entire competitive landscape for AI commerce before Doubao and Qwen have established their footholds.

What Both Sides Haven’t Solved

None of this means American AI companies have figured out the business model. They haven’t.

OpenAI is simultaneously running consumer subscriptions, enterprise licensing, and a newly launched advertising layer. The uncomfortable financial reality is that frontier AI inference has no zero-marginal-cost distribution effect. Every query costs real compute. The company has raised tens of billions in outside capital precisely because it hasn’t yet demonstrated the margin structure of a sustainable business.

Anthropic’s trajectory is the most commercially coherent story in American AI, building toward something that looks more like Salesforce than like a consumer app, with enterprise contracts driving 80% of revenue. But the IPO it has quietly filed for will put that story to a much harsher public test.

Google’s approach embeds Gemini across Workspace, Search, and Cloud as an ARPU multiplier rather than a standalone product. It’s strategically elegant. It also raises the question of whether Gemini is a great business, or just a feature that makes Google’s existing businesses marginally better.

The honest answer on both sides of the Pacific is that nobody has fully solved this yet. The difference is in what stage of unsolved each side is at.

The Real Question

The AI coverage that dominates both Western and Chinese media tends to focus on model benchmarks. Which LLM scores better on reasoning? Who released the biggest context window? Who won the latest eval?

That conversation matters. It’s just not where the industry’s fate is being decided.

The actual question, the one that will determine which companies are still standing in five years, is simpler and harder: who figured out who pays, and why?

Silicon Valley’s answer, imperfect and still evolving: build consumer products to establish trust and brand, then sell to enterprises. The consumer product is marketing. The enterprise contract is the business.

China’s answer, also imperfect and still evolving: acquire users at scale, then route their attention toward commerce. The chatbot is the front door. The transaction is the revenue.

Doubao charging 68 yuan is what happens when a company built on the second logic tries to borrow from the first, in real time, in public, with 345 million users watching.

Silicon Valley is trying to turn AI into software.

China is trying to turn AI into traffic.

History suggests the two eventually converge. The question is who gets there first — and whether the gap in revenue architecture between them closes before it becomes permanent.

| A guest post by

|