How a Stubborn Founder and a Patient City Put China in the Memory Chip Race

Behind CXMT's explosive IPO numbers is something more interesting than a lucky cycle — a decade-long bet between a founder who wouldn't quit and a city that refused to walk away.

On May 17, ChangXin Memory Technologies filed an updated IPO prospectus with Shanghai’s STAR Market. The numbers inside demanded a second look.

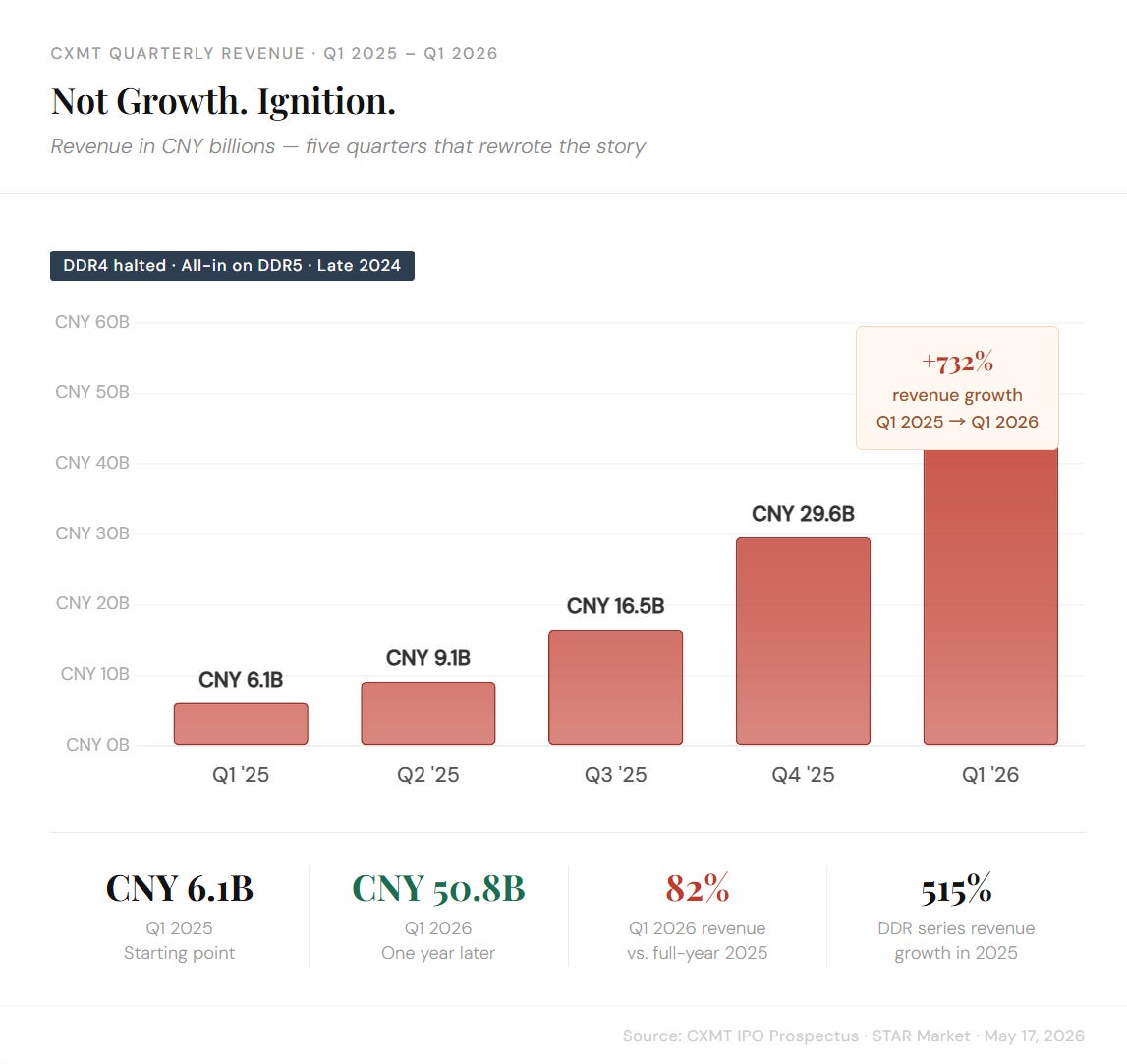

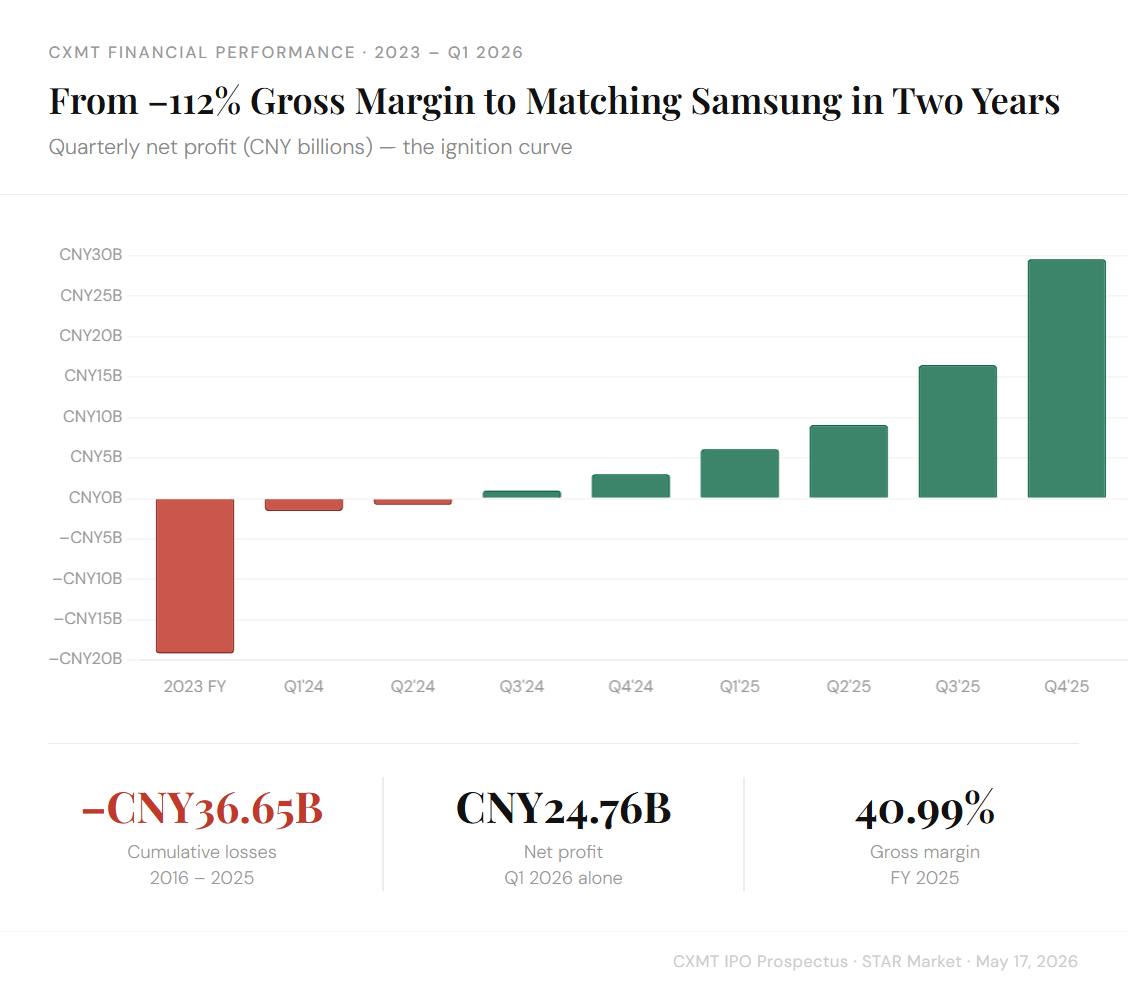

First quarter of 2026: CNY50.8 billion (USD7.5 billion) in revenue, CNY24.76 billion(USD3.6 billion) in net profit. One year earlier, the same company had posted a net loss of CNY1.56 billion(USD230 million ).All figures per CXMT’s updated IPO prospectus, filed May 17, 2026. Its 2025 gross margin reached 40.99%, a number that would have been unthinkable just two years earlier when it sat at -112.71%.

The easy explanation is the AI-driven memory price surge. When the world’s three dominant DRAM makers — Samsung, SK Hynix, and Micron, who together control over 90% of the global market — redirected their best capacity toward high-bandwidth memory for AI servers, they starved the conventional DRAM market of supply. Prices exploded. SK Hynix’s DDR4 production share fell to just 20% by Q4 2024. Samsung shuttered a 24-year-old NAND production line to convert the facility into a DRAM backend factory. On SK Hynix’s Q1 2026 earnings call, management offered a pointed observation: customers are no longer negotiating on price. They just want chips.

There is also a structural twist that made CXMT’s position even more lucrative than it first appeared. HBM, the premium stacked memory that sits beside AI server GPUs, is priced annually. Conventional DRAM reprices every quarter. In a market where prices are rising this fast, the quarterly repricing is actually an advantage. Samsung flagged it directly on its own earnings call: conventional DRAM margins had caught up to HBM. DDR5 and LPDDR5X, the exact products CXMT had pivoted its entire manufacturing base to produce, were suddenly the highest-margin chips in the memory industry.

But none of that explains why CXMT was sitting in exactly the right spot when the cycle turned. That part of the story starts a decade earlier, and it involves two bets made simultaneously: one by a founder, and one by a city.

The Bet They Made Together

In 2016, Hefei and Zhu Yiming found each other because they had the same problem and the same ambition.

Hefei’s anchor industries — home appliances, flat-panel displays, automobiles — were all running into the same wall. They needed chips they couldn’t source domestically. The city had actually been planning around this since 2013, when it set a goal to become China’s “IC capital,” a full year before chip development became a national priority. Its logic was not geopolitical abstraction. It was the practical recognition that its existing industries would stagnate without a domestic supply chain upstream of them. As one Hefei development official put it, the city started thinking about chips because its factories couldn’t find them.

CXMT was not Hefei’s only move. In 2015, the city had brought in a 12-inch wafer manufacturing project through a joint venture with Taiwan’s Powerchip. In 2016, it co-acquired NXP’s standard products division. The city was playing a long game in integrated circuits, and it understood — as Hefei Construction Investment Group chairman Yong Fengshan once described it — that the industry “is like playing Go. It requires years of accumulated positioning.” The goal, as one academic observer put it, was never to transplant a single tree. It was to grow a forest.

Zhu Yiming arrived as the anchor tenant for that forest.

He had spent the previous decade building GigaDevice (兆易创新) from a USD920,000 startup, USD80,000 short of his original target, into a genuine competitor in NOR Flash memory. His approach had always been the same: don’t attack market leaders on their strongest ground; find the flanks, build competence, and use that foothold to climb. He called it “pragmatic innovation,” and it had worked. GigaDevice climbed to become the world’s third-largest NOR Flash manufacturer. But NOR Flash was always a staging ground. The real target was DRAM, the core working memory in every device that computes.

In 2016, the DRAM market was exactly as forbidding as it appeared. Three companies controlled 96% of global supply. China’s domestic production capability was, for all practical purposes, zero. Zhu understood this. He moved anyway.

When he decided it was time to go after DRAM, Hefei was ready to move with him. The city put up three-quarters of Phase One’s capital, roughly CNY13.5 billion (USD1.98 billion) of the CNY18 billion(USD2.64 billion) total, and committed to staying in through whatever followed. That figure sounds large until you consider the scale of what they were attempting. Samsung’s annual capital expenditure in 2021 exceeded USD30 billion. CXMT’s entire Phase One investment was a fraction of that. As the industry saying goes, staying in the DRAM business requires at least CNY10 billion(USD1.46billion) per year just to maintain competitive position. Zhu and Hefei both understood they were beginning a very long march.

Hefei went further than just writing checks. When CXMT needed intellectual property to get started without running into the legal thickets that had trapped other would-be entrants, Hefei helped broker the solution. In 2019, the company acquired a comprehensive patent license from Canadian IP firm Wi-LAN Inc., clearing a critical obstacle that might otherwise have taken years to resolve on its own. That same year, CXMT announced mass production of its first 8Gb DDR4 chip, China’s first domestically manufactured DRAM at commercial scale. One account from the time noted that Kingston and Samsung quietly cut their memory prices shortly after the announcement. The threat had registered.

Provincial and municipal state capital vehicles participated in multiple subsequent funding rounds, bringing in private co-investors alongside them. The ownership structure that emerged reflects just how deeply Hefei embedded itself in the project. The largest shareholder, Qinghui Jidian, is itself majority-owned by entities from the Hefei Economic Development Zone state capital system and the Hefei industrial investment system. The second-largest shareholder, Changxin Integration, is 100% controlled by Hefei’s municipal state-owned assets commission. Some observers have taken to calling Hefei state capital the “de facto controller” of CXMT, and the description is hard to argue with.

Zhu’s personal commitment matched Hefei’s institutional one. He resigned as CEO of GigaDevice, retaining only the chairmanship, took the CEO role at CXMT himself, and made a public pledge to draw no salary or bonus until the company turned a profit. He also pulled key people with him: CXMT’s current president had previously served as GigaDevice’s VP of strategic marketing and was a fellow Tsinghua alumnus. “Throughout the entire project,” Zhu later said, “the provincial and municipal governments provided enormous assistance, forming dedicated leadership teams and supporting construction and financing at every step.”

The technical strategy Zhu brought to CXMT was deliberately aggressive. Rather than climbing the DRAM technology ladder one generation at a time — catching up to where Samsung was three years ago, then two years ago — he designed a “generation-skipping” roadmap. The company would leapfrog intermediate nodes and aim for current-generation competitiveness. This meant heavier upfront research costs, longer timelines to revenue, and significantly higher execution risk. It also meant that when CXMT’s products finally reached maturity, they would be competing against today’s products rather than yesterday’s. From 2023 to 2025, the company spent CNY20.6 billion (USD3.02 billion) on R&D, equal to 21.67% of revenues over that period. Its R&D intensity in 2025 was 15.52%, exceeding Samsung’s 11.31%, SK Hynix’s 6.66%, and Micron’s 10.16%.

Hefei, meanwhile, was not simply waiting. It was building the forest it had promised. Companies including Cambricon, Tongfu Microelectronics, and Paidun Technology set up operations in the area, drawn by CXMT’s anchor presence. Equipment suppliers, materials companies, and packaging and testing facilities clustered around the anchor and grew outward. By 2025, Hefei’s integrated circuit industry output had reached ¥151.4 billion, a 7.4-fold increase from 2016. The city had become one of a handful in China with a complete integrated circuit supply chain spanning design, manufacturing, packaging, and testing.

The pivot that would ultimately define CXMT’s market position came in late 2024, with the losses still recent and the upcycle not yet visible. Zhu made the call: stop all DDR4 production and redirect every fab to DDR5 and LPDDR5X. DDR4 was still the volume market. DDR5 adoption was real but not yet dominant. If the transition happened more slowly than expected, CXMT would be sitting on expensive capacity making products the market didn’t urgently need. It was, by any honest measure, a bet on timing placed on top of a decade of prior bets.

The AI wave arrived instead, and it arrived fast. SK Hynix’s management noted on its Q1 2026 earnings call that AI was rapidly transitioning from large-model training toward inference and Agentic AI, with data volumes growing at every stage of the pipeline, and that this structural demand growth would likely persist for years. Every major Chinese internet and consumer electronics company — Alibaba Cloud, ByteDance, Tencent, Xiaomi, OPPO, vivo — needed more memory than the incumbents could supply. CXMT’s DDR series revenue grew 515% year-over-year in 2025. Its quarterly revenues traced a line that looked less like organic growth and more like ignition: CNY6.1 billion (USD895.5 million) in Q1, CNY9.1 billion(USD1.35billion) in Q2, CNY16.5 billion (USD2.42 billion) in Q3, CN29.6 billion (USD4.34 billion)in Q4. By Q1 2026, a single quarter’s revenue equaled 82% of the entire prior year. Its global DRAM market share reached 7.67% by capacity in Q4 2025, up from 3.97% six months earlier, making it the world’s fourth-largest DRAM manufacturer by capacity and the largest in China, according to the company’s IPO prospectus.

The Years that Looked Like Failure

Between 2016 and 2025, CXMT accumulated losses of CNY36.65 billion (USD5.38 billion). During the brutal 2022-2023 DRAM downcycle, when global prices fell 50% from their peak, the company posted a net loss of CNY19.2 billion (USD2.81 billion)in a single year and took CNY11.5 billion (USD1.68 billion) in inventory impairment charges. Its gross margin hit -112.71%. It was spending more than twice the selling price of its chips just to manufacture them. Samsung, SK Hynix, and Micron all cut production utilization rates during that same period to protect their margins. It was the rational move.

CXMT did the opposite. It kept expanding.

The prospectus describes the decision in plain language: “sustained capacity expansion to ensure revenue growth and market share expansion.” What it doesn’t capture is what that decision cost, or what it required of the people making it. Zhu’s team was absorbing the fixed costs of three 12-inch wafer fabs while selling products below cost. Hefei’s state capital vehicles were watching their investment accumulate losses with no visible timeline for recovery. There was no obvious reason, from the outside, to believe the situation would ever look different.

Neither party blinked.

What kept Zhu going was the same conviction that had driven every move he’d made since GigaDevice’s founding: that the technology gap could be closed faster than conventional wisdom suggested, if you were willing to invest in closing it while everyone else was hunkering down. Hefei’s patience was grounded in a different but compatible belief — that industrial capability is not built in a single budget cycle, and that walking away during the losses would not just end CXMT but unravel the entire ecosystem forming around it. The anchor had to survive.

By the end of 2025, the three fabs were running at 95.7% utilization. Every wafer coming off the line was being absorbed immediately by orders. The gross margin that had sat at -112.71% in 2023 had reached 40.99% in 2025, above Samsung’s 39.38% in the same period. From the floor to shoulder-to-shoulder with the world’s largest memory company, in two years.

What the IPO is Really Saying

The CNY29.5 billion (USD4.3 billion) CXMT is raising in this IPO is not distress capital. The company generated CNY42.57 billion (USD6.24 billion) in operating cash flow in Q1 2026 alone. The raise is about what comes next: process upgrades, manufacturing line improvements, and CNY9 billion (USD1.32 billion) for advanced R&D, including continued work on HBM, where CXMT reportedly has samples in delivery.

The listing matters for a reason beyond CXMT’s own balance sheet. China’s AI-related equity market is currently dominated by optical module makers, server assemblers, and PCB manufacturers, companies that sit downstream from the chip supply chain. They benefit from AI investment, but their margins are ultimately constrained by what the chip companies charge them. They are, in the blunt framing of one analyst, drinking the soup from a pot they don’t control.

CXMT is the pot. It is the first Chinese company to sit at the upstream end of the memory value chain, designing its own chips, manufacturing them at scale, and capturing the margin rather than being subject to it. When it lists, it will likely become the largest company on the STAR Market.

The gap to the incumbents is real and should not be minimized. Samsung, SK Hynix, and Micron together still hold over 92% of global DRAM market share. CXMT is producing at 16nm without EUV lithography, while the leaders manufacture at 12-14nm with it, a gap of roughly three years that will not close easily. CXMT’s own prospectus is candid about this distance.

But gross margin doesn’t lie, and 40.99% above Samsung’s 39.38% is the number that matters most right now. It means that in 2025, CXMT was manufacturing memory chips with a level of efficiency and product sophistication that matched the company that has dominated this industry for thirty years.

The story people will tell about CXMT is that it caught a cycle. That prices happened to surge when CXMT happened to have DDR5 capacity ready, and that the company got lucky.

That story isn’t wrong. Timing mattered enormously.

But it leaves out the part where a founder pledged his salary for ten years and kept spending on R&D through a downcycle that would have justified cutting. It leaves out the part where a city co-signed that bet, not just with capital but with patent deals, ecosystem-building, and the kind of institutional patience that most investors, public or private, cannot sustain past the first few bad quarters. It leaves out the decade of decisions — the generation-skipping roadmap, the DDR4 exit, the counter-cyclical expansion — each one defensible, none of them guaranteed, all of them necessary.

| A guest post by

|