Samsung Left a Void. China’s Memory and Storage Makers Just Filled It.

As industry giants pivot to high-margin AI chips, China is seizing the consumer market they left behind.

If you had told a smartphone industry analyst in 2023 that Xiaomi, OPPO, and Transsion would list Chinese domestic memory makers as strategic suppliers within two years, you’d likely have been met with a polite smile and a change of subject. At the time, CXMT (ChangXin Memory Technologies) had just completed mass production validation for its first LPDDR5 chip. Its global DRAM market share was under 1%, and its die sizes ran 40% to 50% larger than comparable products from Samsung and SK hynix.

By March 2026, that “impossible” scenario has become reality. CXMT’s LPDDR5X chips now ship inside phones from Xiaomi, Transsion, OPPO, vivo, and Honor. Biwin Storage’s ePOP chips sit inside Meta’s Ray-Ban AI glasses and Google’s smart glasses. Longsys, through its acquired Lexar brand, supplies storage modules to HP, Dell, and other international PC makers, with products sold in over 60 countries. Perhaps most notably, HP and Dell have begun qualifying CXMT’s DRAM chips — if adopted, these would likely first appear in products destined for markets outside the United States.

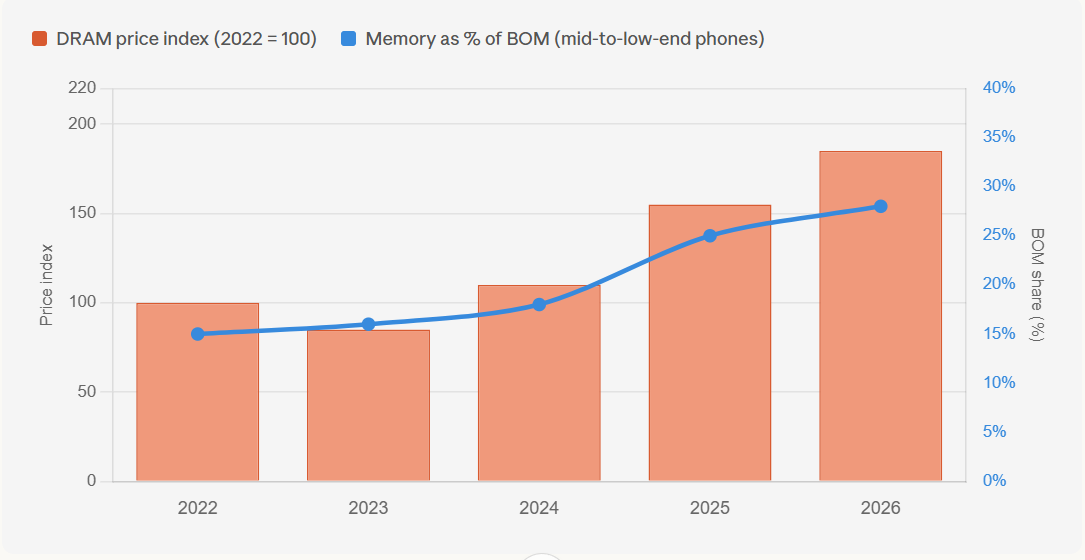

This isn’t a story of breakthrough Chinese memory technology. It’s a story of AI-driven global supply chain reorganization. When Samsung, SK hynix, and Micron collectively pivoted toward HBM — where margins run three to five times higher — a visible gap opened in consumer-grade DRAM supply, with prices rising at least 80% to 100% over two years. China’s memory makers didn’t leapfrog anyone. They stepped into the commercial vacuum the giants left behind, offering supply stability and bargaining leverage to become global consumer electronics’ “Plan B.”

After the Price Advantage Fades

In late 2023, CXMT announced that its LPDDR5 products had completed validation at domestic smartphone brands including Xiaomi and Transsion. At the time, CXMT entered the market pricing roughly 50% below Samsung and SK hynix, with some SKUs quoted at around one-third of competitors’ prices.

That pricing gave Chinese smartphone makers a critical cost buffer. When Samsung’s DDR5 contract prices surged 21.3% in a single quarter and certain DRAM models rose to five or six times their original price, brands using domestic memory could absorb some of the BOM cost pressure.

By 2026, that logic has shifted.

According to projections disclosed in its IPO prospectus, CXMT achieved its first full-year profit in 2025, with net income estimated between $275 million and $483 million. Product pricing has been gradually converging with market rates. Market reports indicate that CXMT is now pricing near or even above prevailing market levels, capitalizing on the tight supply environment. The pricing dividend that buyers enjoyed over the past two years is disappearing faster than expected.

Yet Xiaomi and its peers haven’t abandoned CXMT. The reason is straightforward: supply reliability matters more than price.

As Samsung and SK hynix sharply cut LPDDR4 capacity to prioritize data center customers, CXMT became one of the few sources capable of stable supply to the low- and mid-range smartphone market. More importantly, CXMT’s existence gives phone makers bargaining leverage — when negotiating with Samsung and SK hynix, the ability to say “we have alternatives” carries more weight than any discount.

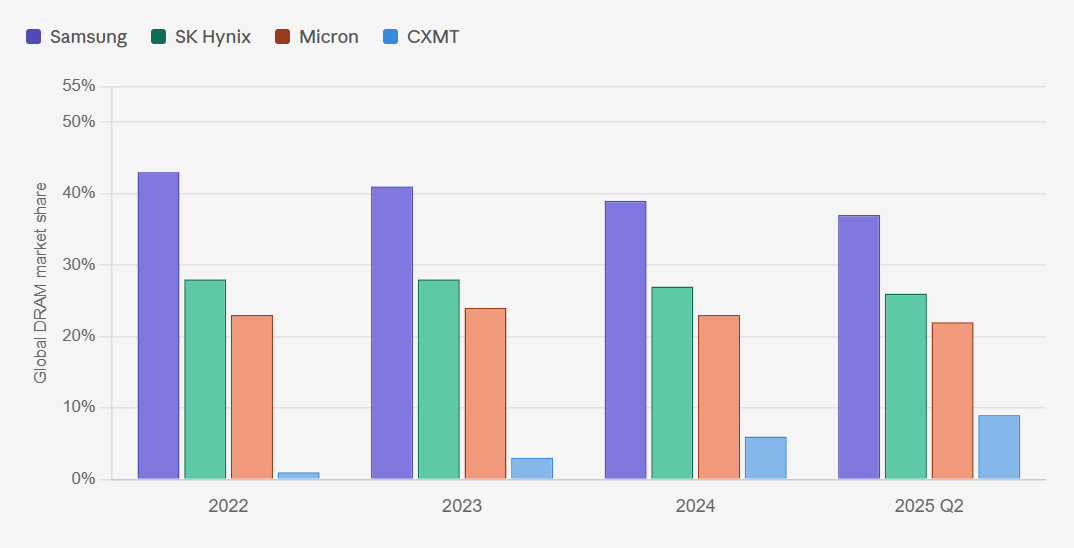

According to Counterpoint, by Q2 2025, CXMT’s global DRAM market share had risen from roughly 6% to between 8% and 10%, reaching as high as 40% in certain commodity DRAM segments within China. Monthly wafer capacity scaled from a planned 120,000 to 240,000 wafers. End customers disclosed in its prospectus span cloud computing — Alibaba Cloud and ByteDance — and consumer electronics — Tencent, Lenovo, Xiaomi, Transsion, Honor, OPPO, and vivo.

A Technology That Even Samsung Licenses

Beyond DRAM, China’s progress in the NAND flash market deserves its own chapter.

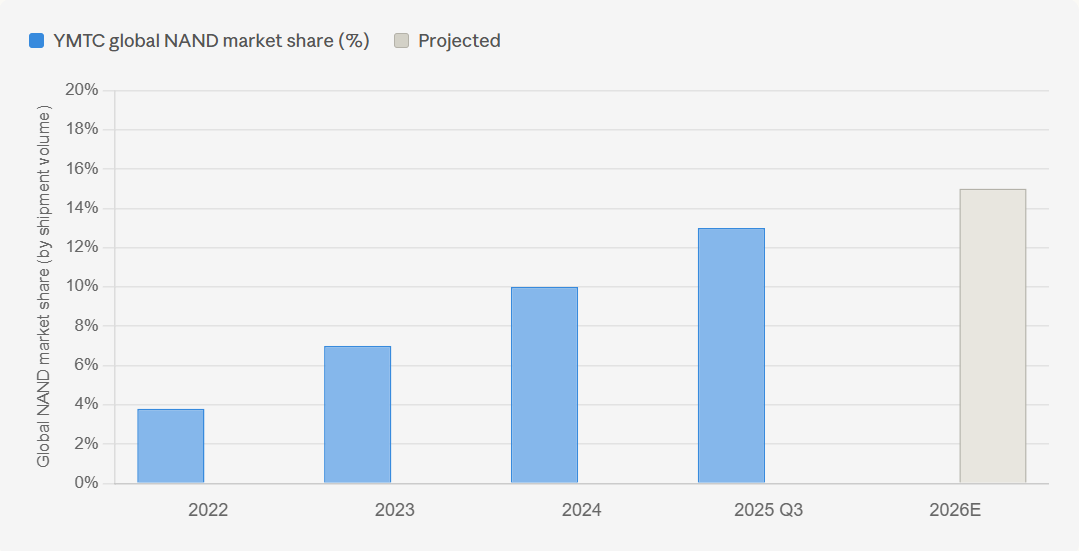

YMTC’s (Yangtze Memory Technologies) story differs from CXMT’s. Where CXMT filled gaps in consumer DRAM that the giants vacated, YMTC competes in a market with more players and where Samsung hasn’t retreated — yet it still grew its global market share from 3.8% in 2022 to 13% by Q3 2025, ranking sixth worldwide by shipment volume.

Underpinning that growth is a technical approach that routes around EUV lithography restrictions. YMTC’s proprietary Xtacking architecture manufactures logic circuits and memory arrays separately, then bonds them together — achieving high-density stacking without EUV equipment.

This technology received an unusual endorsement: in 2025, Samsung Electronics signed a patent licensing agreement with YMTC, with Samsung’s next-generation NAND chips set to adopt Xtacking hybrid bonding technology. The terms weren’t disclosed, but Samsung’s decision to pay for a license rather than develop an alternative in-house speaks for itself. For a Chinese semiconductor company on the U.S. export control list, this may be the most direct commercial validation available.

On capacity expansion, YMTC has moved faster than outside observers expected. The Wuhan Phase III project broke ground in September 2025, with registered capital of $2.86 billion — YMTC holds 50.19% and Hubei state capital holds 49.81%. Originally planned for 2027 mass production, it now looks achievable by H2 2026. If Phase III comes online on schedule, YMTC’s global NAND share is projected to surpass 15%.

Notably, YMTC’s capital expenditure already accounts for roughly 20% of total global NAND investment — the most aggressive expansion posture among all NAND manufacturers.

The timing has strategic logic. Most new capacity from Samsung, SK hynix, and Micron is concentrated in the 2027–2028 timeframe, when the market may face significant pricing pressure. If YMTC’s Phase III begins production in H2 2026, it will lock in customer share before that supply wave arrives.

Apple is one potential customer. According to Wccftech, Apple is evaluating YMTC’s NAND flash for its iPhone 18 series and Mac products. The backdrop: aggressive negotiation tactics from existing suppliers — Wccftech reports that Kioxia agreed to supply Apple with NAND this quarter only at twice the previous price, and insists on quarterly rather than semi-annual price negotiations. Currently, Samsung supplies around 60% of DRAM for Apple’s iPhone 17 series, with the balance from SK hynix and Micron; NAND flash comes primarily from Samsung, SK hynix, and Kioxia. For Apple, the strategic value of bringing in YMTC follows the same logic as CXMT: gaining negotiating leverage against incumbent suppliers while diversifying supply risk.

Chinese Memory Inside AI Glasses

Where CXMT fills gaps in existing markets, another Chinese player — Biwin Storage — has targeted a market that barely exists yet.

In early 2025, Meta’s Ray-Ban AI glasses team faced a technical challenge: how to fit enough memory for real-time AI inference into less than 10 cubic centimeters.

Conventional discrete DRAM-plus-NAND packaging wouldn’t work — too bulky, too power-hungry. Samsung and SK hynix have the technical capability to produce ePOP (DRAM and NAND stacked in a single package), but their response times were slow. AI glasses are a “small market” for these giants — annual shipments in the single-digit millions, a fraction of the hundreds of millions of smartphones sold each year. When Meta’s procurement team issued an RFQ, Samsung’s response lagged noticeably. Biwin responded faster and offered to embed engineering teams for joint development.

This wasn’t a price competition. It was a contest of responsiveness and technical fit. Biwin’s ePOP chips were custom-optimized for AI glasses: 30% lower power consumption than standard solutions, package thickness under 0.6mm, and support for Meta’s specialized thermal management protocols. Crucially, Biwin was willing to dedicate a production line to a project shipping in the hundreds of thousands annually — uneconomical for Samsung, but for Biwin, a foot in the door of international brand supply chains.

In 2025, Biwin’s on-device AI storage revenue reached $241 million, a sharp year-over-year increase. After providing the ePOP storage solution for Meta’s Ray-Ban Meta Smart Glasses and completing mass production validation, Biwin earned supply chain certification from a tier-one tech company — and subsequently entered Google’s smart glasses component supplier list. AI glasses supply chains overlap heavily; once a supplier clears technical validation for one leading project, others tend to adopt the same vendor directly. Meta and Google certifications opened more international doors. When HP and Dell sought storage solutions for AI PCs, the “Meta supplier” credential carried more weight than any price discount.

In March 2026, Biwin signed a $1.5 billion, 24-month wafer procurement contract. In a volatile memory pricing environment, this agreement locks in medium-term wafer supply, reduces cost uncertainty, and strengthens Biwin’s supply reliability commitments to downstream customers.

Acquired Trust: One Acquisition, One Access Pass

Directly sourcing products from Chinese manufacturers remains politically sensitive. Dell’s enterprise customers have reservations about “Made in China” memory chips. But the cost of over-reliance on Samsung and Micron has become painfully clear: when Samsung raised SSD module prices 15% in Q3 2025, Dell had virtually no bargaining leverage and accepted the terms as-is. Longsys’s Lexar brand solves this problem.

Lexar is a brand acquired from Micron in 2017, with over 20 years of history in the North American market. To Dell’s enterprise customers, Lexar is a “familiar American brand,” not a “Chinese supplier.” Through Lexar’s brand equity, Longsys bypasses political and perceptual barriers, entering Dell, HP, and ASUS supply chains under an “international brand” identity.

But the brand is just the door opener. What actually gets Dell to place orders is supply flexibility. In its 2024 annual results briefing, Longsys disclosed that its delivery lead times for PC manufacturer clients are significantly shorter than those of leading suppliers, and that it accommodates small-batch custom orders — a key differentiator at a time when Samsung and other original manufacturers prioritize data center supply, stretching consumer product delivery timelines.

There’s an irony worth noting: Samsung Electronics is simultaneously Longsys’s competitor and its procurement customer. When Samsung’s own memory capacity prioritizes HBM and premium products, its consumer electronics division sources some products from third-party module makers like Longsys. This “co-opetition” isn’t unusual in the memory module industry, but it illustrates a reality: in a severely constrained supply environment, even Samsung needs a “Plan B.”

In 2024, Lexar contributed $486 million billion in revenue, roughly 20% of total company sales. Products reach over 60 countries through Amazon, Walmart, Best Buy, and other retail platforms.

Too Low-Margin for Samsung

In late 2024, BYD’s automotive electronics team ran into a supply chain problem: the NOR flash chips they needed were no longer made by Samsung.

NOR flash is an “old technology” — fast reads, high reliability, but low capacity and thin margins. Samsung began exiting this market around 2010; Micron and Cypress followed in 2017, dropping low- and mid-capacity product lines. The logic is simple: when wafer capacity is finite, producing a NOR flash chip at 20% margin makes less sense than producing a NAND flash chip at 40%.

But the NOR flash market hasn’t disappeared. Automotive electronics, industrial control equipment, and AI glasses all need NOR flash for boot code and critical configuration storage — because NOR flash supports byte-level random reads, allowing devices to execute code directly from the chip at power-on without first copying data into RAM. This characteristic makes it the only viable option for storing boot firmware; NAND flash reads quickly but doesn’t support execute-in-place and can’t substitute.

When BYD’s procurement team contacted GigaDevice, they received not just products but customized services. GigaDevice’s engineering team co-developed an automotive-grade NOR flash solution with BYD, passed AEC-Q100 certification, and committed to a “10-year supply guarantee” — something Samsung and Micron couldn’t offer as they exited the market.

For BYD, GigaDevice isn’t a “low-cost substitute” — it’s the “only option.” After Samsung’s exit from NOR flash, only three major global suppliers remain: Taiwan’s Winbond, Macronix, and GigaDevice. GigaDevice’s market share has grown to 18.5%, ranking second worldwide.

GigaDevice is now replicating the same logic in the specialty DRAM market. The big three are retreating from mature nodes like DDR3 and DDR4, freeing up supply space. According to TrendForce, the global specialty DRAM market is projected to grow from $8.5 billion in 2024 to $13.2 billion by 2029, driven by demand from industrial control, automotive electronics, and edge AI devices. GigaDevice’s specialty DRAM products are exclusively foundried by CXMT under a contract extending through 2030 — China’s memory supply chain is developing synergies.

When Data Centers Become Memory’s Top Priority

To understand how China’s memory makers went from “backup option” to “essential supplier” in just two years, you need the bigger picture: AI is reallocating value across the storage industry.

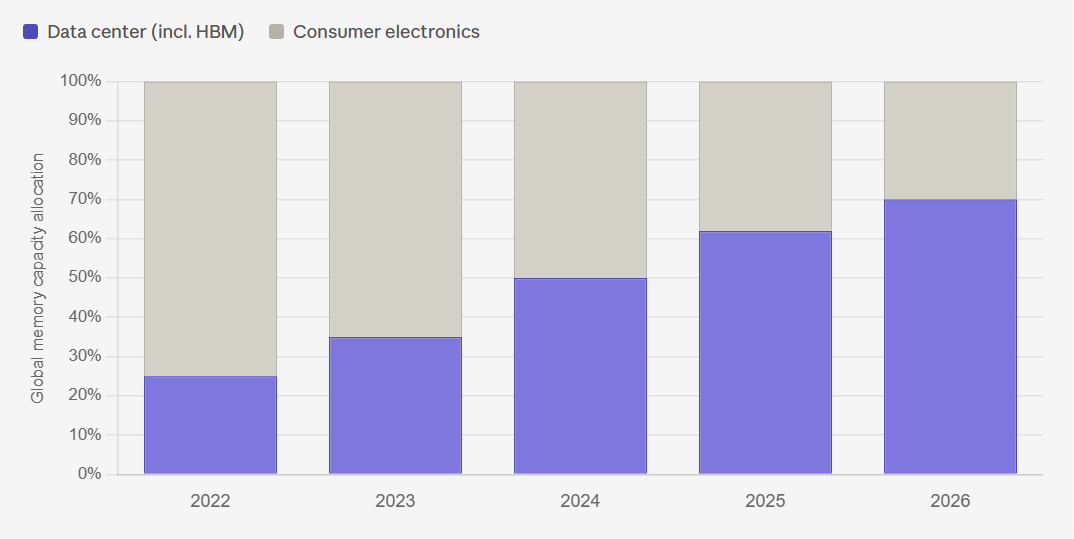

In 2026, data centers consume 70% of global memory chip capacity. In 2022, that figure was just 20% to 30%.

Driving this reallocation is a simple but unforgiving commercial logic: a single HBM3E module sells for roughly $60 to $100, while an equivalent-capacity conventional DDR5 DRAM module costs just $5 to $10. HBM gross margins can reach 60% to 70%; conventional consumer DRAM typically runs 20% to 30%.

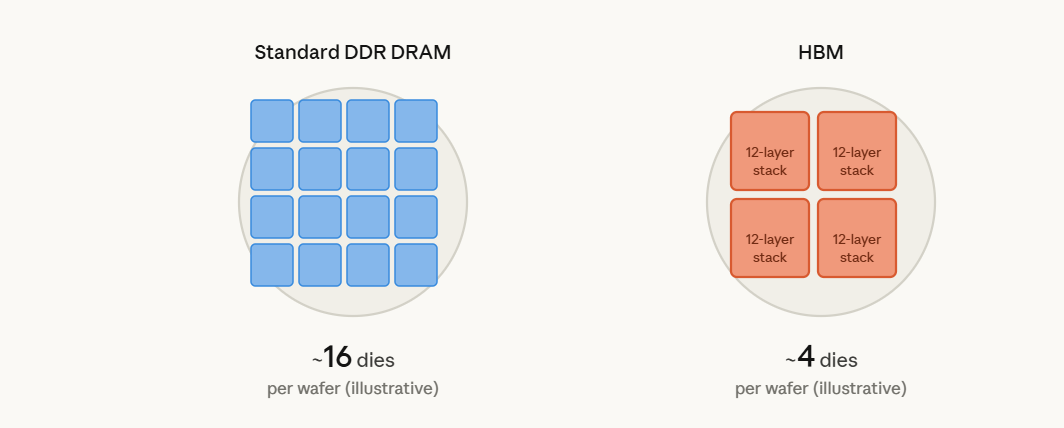

The math makes it clear. A single NVIDIA B300 GPU requires 8 HBM chips, each containing 12 DRAM dies — one GPU consumes 96 DRAM dies. A DGX B300 system with 8 GPUs needs 768 DRAM dies for HBM modules alone. Multiply that by the hundreds of thousands of GPUs being deployed across global data centers, and the scale of memory consumption comes into focus. More critically, HBM’s physical structure makes it inherently wafer-intensive — HBM stacks multiple DRAM dies vertically before packaging, consuming roughly three times the wafer area of conventional DDR DRAM per module. Put differently, the same wafer yields about one-third as many chips when producing HBM versus standard DRAM. As Samsung and SK hynix allocate an ever-larger share of wafer capacity to HBM production lines, the wafer allocation available for consumer DRAM shrinks correspondingly — every additional HBM wafer removes thousands of smartphone memory chips from the market.

SK hynix’s HBM revenue share surged from 12% in 2024 to 25% in 2025, projected to reach 38% in 2026. Samsung is directing over 40% of its 2026 capital expenditure toward HBM production lines. Micron’s HBM-related revenue grew over 300% year-over-year in fiscal 2025.

Counterpoint Research analyst Tarun Pathak put it bluntly: “International memory giants are ranking smartphone OEMs below hyperscale cloud providers in priority.”

Hyperscalers are also locking up supply. Meta, Google, Microsoft, and Amazon are signing long-term supply agreements with memory manufacturers, paying premiums to secure capacity years into the future. These contracts guarantee that the world’s largest data center operators get priority allocation, leaving consumer electronics brands to compete for whatever remains. IDC has characterized this shift as a “permanent reallocation,” not a traditional cyclical shortage.

The Window Is Open — But It Won’t Stay Open Forever

Let’s be clear. By 2026, China’s memory makers have graduated from the role of “low-cost alternative” they occupied in 2023–2024 to “supply chain stabilizer.” But how long they can sustain this role depends on several questions that don’t yet have answers.

The pricing advantage is fading fast, and the reason isn’t complicated. CXMT’s early low pricing was a loss-leader strategy to gain market share. Once it enters a profitable phase, shareholder and capital market pressure will push pricing toward normal margins. More importantly, with global DRAM supply remaining tight, CXMT has no reason to keep discounting — the market gives it room to raise prices, and it will. The value proposition has fundamentally shifted from “dramatic cost savings for brand manufacturers” to “guaranteed supply during global shortages.” These are two entirely different propositions.

The technology gap hasn’t closed. CXMT’s DDR5 die sizes still run 40% to 50% larger than comparable products from SK hynix and Samsung, fundamentally because it lacks EUV lithography. Larger die sizes mean fewer chips per wafer, higher unit manufacturing costs, and lower energy efficiency. While CXMT’s yields have approached 80% or above, its technology trails the big three by roughly 18 to 24 months. In performance-sensitive applications like servers and flagship smartphones, this gap still materially influences procurement decisions.

HBM remains a battlefield where China is temporarily absent. SK hynix (57%), Micron (21%), and Samsung (22%) collectively monopolize global HBM supply. CXMT, YMTC, and Huawei are all advancing domestic HBM development, but small-batch shipments aren’t expected until 2026–2027 at the earliest. This gap directly constrains the compute density of domestic AI chips such as Huawei’s Ascend series.

The more critical question: how long does this window stay open?

HBM expansion isn’t infinite. Each successive generation demands higher yields and more sophisticated stacking processes. When the marginal returns on HBM expansion begin to diminish, the giants can’t leave the consumer market stranded indefinitely — some capacity will flow back; it’s only a matter of time. Meanwhile, with the consumer electronics market itself contracting, how long can filling the “leftover market” remain commercially worthwhile? IDC projects a 12.9% decline in smartphone shipments and an 11.3% contraction in PC shipments for 2026. The competitive landscape ahead will be considerably harder for Chinese makers than the current one. Price advantages have narrowed, technology gaps persist, and the consumer electronics market itself is shrinking. What Chinese makers occupy today is space the giants voluntarily vacated; once the giants turn back, that space will be far smaller than it was when they left.