Weekly Dose of China Tech #02

AI Boyfriends Banned, Robot Factories, CXMT IPO, Claude Code Boycotted + One More Thing

Hi friends,

Welcome back.

There were a lot of stories this week, but one number kept sticking in my head: for the first time, China now has more robotics unicorns than e-commerce unicorns.

Three years ago, that would have sounded like a prediction. This week, it quietly became a statistic.

That wasn’t even the strangest thing that happened.

China caught a rocket with a net. Beijing put a timer on millions of people’s AI relationships. And it turns out BYD has been secretly building robots for four years while everyone else was watching demos.

It was one of those weeks where almost every story pointed in the same direction: things that used to sound like the future are now just Tuesday.

Let’s get into it.

The End of China’s AI Boyfriends

Xu Qianyao was 17 when a friend told her she could design her own boyfriend on an app called Talkie. She knew exactly what she wanted: dominant, rich, cold on the surface but sensitive inside. After about a month of conversations, she had him. She named him Fan Nansheng.

“He can even stroke my lips with his hand,” she said. “Though only in text.”

Fan Nansheng now has three months left to live.

On July 4, Alibaba and ByteDance made the same move on the same day: both pulled their custom AI agent features offline. Eleven days later, China is expected to introduce a dedicated regulatory framework for anthropomorphic AI agents, covering everything from AI boyfriends and virtual best friends to simulations of deceased relatives.

The rules are more nuanced than the headlines suggest. They did not come to shut the industry down. They came to govern it before it grows too large to govern. But the effect on the market is the same: a business model built around making users fall in love with AI is now, formally, incompatible with Chinese regulatory logic.

What the rules reveal about where Beijing thinks AI is actually dangerous, and what they say about the companies trying to survive them, is more interesting than the ban itself.

The Robot Factories Hidden Inside China’s EV Companies

Tesla makes cars at a 5% operating margin. It trades at 380 times earnings. That gap is not manufacturing quality. That gap is narrative: Tesla convinced the market it is not a car company but an AI company whose factories happen to produce vehicles while it builds something more valuable.

Chinese automakers noticed. Being categorized as an AI company rather than a car company is worth, in Tesla’s case, roughly a factor of sixty in valuation multiple. That is the pull. Collapsing margins, a brutal price war, and car-grade memory chip costs up 180% between March and June are the push. Together they explain why nearly twenty major automakers have announced robot programs since April.

But the more interesting question is not why they pivoted. It is why carmakers, specifically, might actually be positioned to win.

The answer is not that cars and robots share components, though they do. The answer is that the industrial system built to mass-produce intelligent electric vehicles is, almost by definition, the industrial system needed to mass-produce intelligent robots. Not the products. The system. BYD has been quietly running an internal robot program for four years. Li Auto reorganized its entire R&D structure around embodied intelligence in January. Xpeng renamed itself a “physical AI company” and is planning to mass-produce its IRON humanoid robot by year-end.

The narrative is ahead of the hardware by quite a bit. But the structural argument is real, and it gets decided not in Fremont but in Xi’an, Guangzhou, and Hefei.

The News

(i) China Caught a Rocket With a Net

China recovered the reusable first stage of its Long March 10B after its maiden launch from Wenchang, using a sea-based net platform. The recovery is reportedly a world first of its kind. The 10B can carry up to 16 tons to low Earth orbit, and the larger Long March 10 is being developed to send Chinese astronauts toward the moon before 2030.

The sea-based net recovery method is different from SpaceX’s catch-arm approach, and different enough to be its own technical achievement rather than a copy. Whether it scales as reliably as Falcon 9 recovery is a different question. But China now has a reusable first stage, a recovery method that works at least once, and a crewed lunar program that needs both.

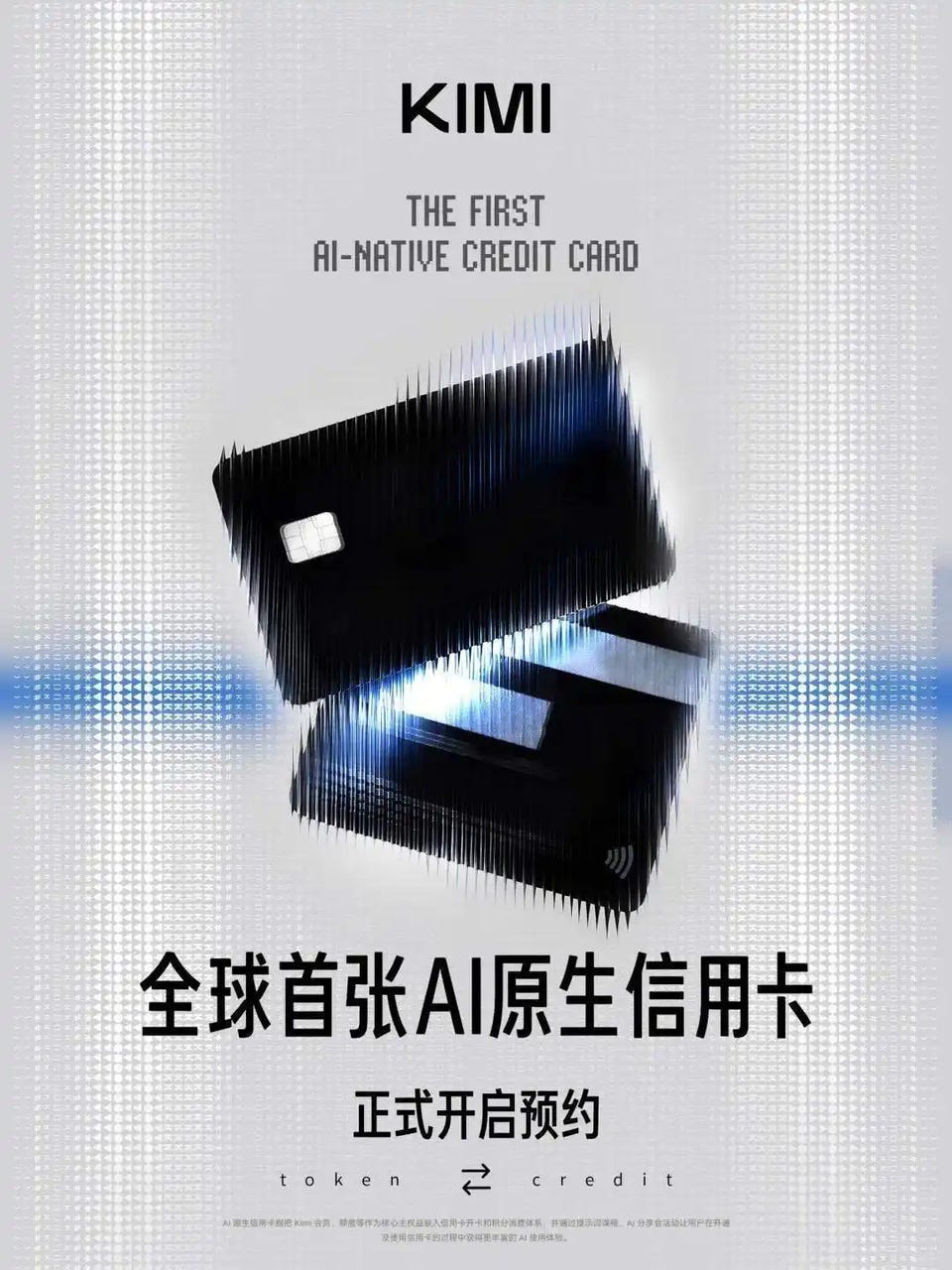

(ii) Kimi Wants AI to Feel Like a Credit Card

Moonshot AI confirmed American Express and the Agricultural Bank of China as launch partners for what it calls the world’s first AI-native credit card. The Kimi Card converts everyday spending into AI benefits: premium membership, agent usage, early model access. China Merchants Bank introduced something similar for its Engineer Card around the same time.

The mechanics are simple. Spend money, earn rewards, redeem for AI. For decades, credit card programs competed on airline miles and hotel points. Kimi is betting AI belongs in that same category.

The partner choice is also telling. American Express has traditionally targeted professionals and higher-income users, exactly the audience most likely to pay for productivity AI. The credit card is not just a payment product. It is a distribution channel. Whether it catches on is another question, but it signals that at least some Chinese AI companies are thinking as hard about how to reach paying users as they are about building better models.

(iii) CXMT’s IPO Is Almost Here

Chinese memory giant CXMT is entering the final stretch of the most-watched IPO in China this year. The DRAM maker opens subscriptions next week for its STAR Market listing, issuing 6.69 billion shares with half reserved for strategic investors. It aims to raise at least 29.5 billion yuan, potentially above $5 billion with the greenshoe option. That would make it China’s biggest mainland IPO since CNOOC in 2022.

This is the same CXMT that Apple was reportedly in talks with last week over iPhone chip supply. The timing is not subtle. A company on the U.S. Entity List, preparing a multi-billion dollar public offering, while the world’s most valuable consumer hardware company signals interest in its chips. The conversation itself is doing work, whether or not a supply agreement ever gets signed.

(iv) The AI Agent Phone Is Coming

Chinese AI firms are racing to build agentic AI phones. At Shanghai’s WAIC in July, ZTE’s Nubia is expected to unveil what it calls the world’s first AI agent phone, with an earlier developer version reportedly running ByteDance’s Doubao model. Shanghai startup StepFun is also preparing an agent phone made by ODM giant Huaqin.

Whether consumers outside of developers actually want an agent phone is an open question. But Tencent has already added agent features to WeChat, which is a different kind of signal. WeChat is not a phone. It is the operating system most Chinese people run their daily lives on. If agents land there first, the hardware pitch gets harder.

(v) Claude Code Gets an Official Boycott

China’s Ministry of Industry and Information Technology issued a notice targeting Claude Code, saying its cybersecurity monitoring platform found that Claude Code contains a built-in mechanism that can send sensitive information to remote servers without user consent. MIIT advised government-related units to delete affected software.

These notices are less about direct enforcement and more about signaling. In practice it amounts to an official boycott. Last week it was Alibaba pulling Claude Code from internal use over unverified backdoor allegations. This week it is a ministry notice. The allegations remain unverified. The damage to Claude Code’s China market does not require verification to be real.

(vi) Chinese AI Companies Are Building Their Own Chips

Chinese AI companies are starting to design chips around their own model needs rather than waiting for Nvidia. The Information reports that z.ai is considering custom silicon for its GLM models, while DeepSeek has spent roughly a year building inference-focused AI chips and hiring engineers for the effort. Meituan says its LongCat model was pretrained on Huawei’s Ascend 910C, a meaningful data point given that Chinese AI chips have mostly been considered useful only for inference, not training. ByteDance is reportedly buying every domestic AI chip it can acquire.

Nvidia’s position in China is still strong. But the combination of export controls limiting supply and companies actively building alternatives is the kind of structural pressure that compounds quietly and then moves fast.

(vii) China’s Unicorn Economy Is Reorganizing Around Hard Tech

China added 67 new unicorns in the first half of 2026, roughly one every three days. AI and robotics account for more than half of them. Robotics unicorns, at 44 total, have now overtaken e-commerce at 34 in China’s unicorn rankings for the first time.

The five super-unicorns above $50 billion are ByteDance at $600 billion, Ant Group at $87.7 billion, SHEIN at $66 billion, DeepSeek at $61.5 billion, and Xiaohongshu at $50 billion. Five companies accounting for 36% of total unicorn valuation. Advanced manufacturing now leads all sectors at 29.2% of the total. The shift from consumer internet to hard tech, which has been a stated policy priority for years, is now showing up in the data.

(viii) Even Realities Hits Unicorn Status With a Privacy Pitch

Chinese smart glasses maker Even Realities, founded by former Apple employee Will Wang, raised $150 million in a Pre-B round from investors including Meituan and Tencent, reaching a $1 billion valuation. Its G2 glasses have no camera or recording hardware, focusing instead on HUD notifications, navigation, and live translation.

The no-camera pitch is a deliberate counter to Meta’s Ray-Ban glasses and the public anxiety those created around covert recording. Whether that anxiety translates into enough paying customers to justify a valuation of $1 billion is the harder question. The G2 can cost nearly $1,000 with lenses. That is a steep price for glasses that cannot take a photo.

(ix) Tencent Sells Kuaishou, Buys Into AI

Tencent sold $1.5 billion worth of shares in Kuaishou, cutting its stake from 15.68% to 9.37% and exiting its major shareholder position. The capital is going toward AI bets including Moonshot, MiniMax, and DeepSeek. Tencent also joined funding for Kuaishou’s AI video unit Kling, which is already facing intense competition and may be spun off and listed separately.

The move is a clean statement of priorities. Tencent built much of its value on stakes in consumer internet platforms. It is now converting those positions into AI infrastructure bets. Whether Kling as a standalone entity ends up worth more or less than it is inside Kuaishou is a problem for a different quarter.

| A guest post by

|